The fund’s performance in December was 6.5%, surpassing the benchmark by 3.3%. One factor behind the robust stock market rally during the month was that market interest rates fell owing to decent inflation data and expectations of interest rate cuts in 2024. This led to increased interest in shares, particularly those that have had a tough 2023, such as real estate, consumer, and small caps. We also note that our global fund delivered stable returns both when the dollar was strong and when it weakened.

The stocks that performed the best during December were Sterling Infrastructure, Sika, and Balder. The three weakest performers were United Health, Ferrari, and Adobe.

It was a relatively quiet period for quarterly reports, with the third quarter releases largely out of the way. There is one report worth noting, though: from software company Adobe. The report was as expected and the company announced the termination of its Figma acquisition after the competition authorities declined to approve the deal. We do not consider this negative for Adobe since the company has good momentum in its business thanks to new AI products.

Key market events and trends (what has influenced performance most?)

During December, the US 10-year bond yield fell from around 4.3% to about 3.9%. The market continued to discount coming interest rate cuts by the Fed, which proved a catalyst for a stock market upswing. The latest inflation reading in the US was around 3.1%, still closing in on the Fed’s 2% target. When inflation falls demonstrably, there will be no reason for the Fed to maintain key interest rates at the high 5.5%, and these are likely to be reduced. At the time of writing, the futures market indicates that the Fed Funds Target Rate will be at some 4.5% in August 2024. If the market is right, there will probably be four reductions of 0.25 percentage points during the year’s first three quarters.

Lower interest rates will benefit the real economy, aiding a recovery in the real estate market. Lower interest expenses will give us more money in our wallets, meaning that car sales, consumption, and vacation travel, among others, will increase. In an environment with falling interest rates, rate-sensitive stocks will perform.

Portfolio changes

We made no changes to our portfolio during December.

The fund’s positioning—our market expectations

Our market belief for late summer and fall 2023 was that inflation would minimize, leading to market interest rates coming down, too. We were right in this forecast, and the market’s interest in “risky” rate-sensitive assets, such as real estate, was considerable during November and December. The returns from our real estate stocks in the Special Situations part of the fund were around 51% in Balder and about 31% in Vonovia during these months. Our Special Situations, with cheaper stocks, still experience a valuation gap through which we can earn money. Among our Champions, profit and revenue growth are what push stock prices up over time. We believe this mix of growth and value cases gives rise to an attractive portfolio that produces appealing returns for unitholders over the long term.

We thank you for entrusting your capital to us and look forward to a thrilling investment year in 2024.

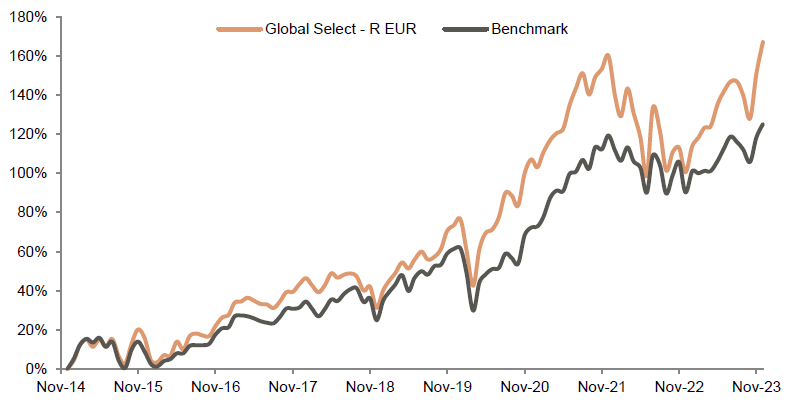

| Mth | YTD | 3 yrs | Since incep | |

| Coeli Global Select – R EUR | 6,47% | 33,15% | 28,97% | 166,99% |

| Benchmark | 3,16% | 18,30% | 30,66% | 125,11% |

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026