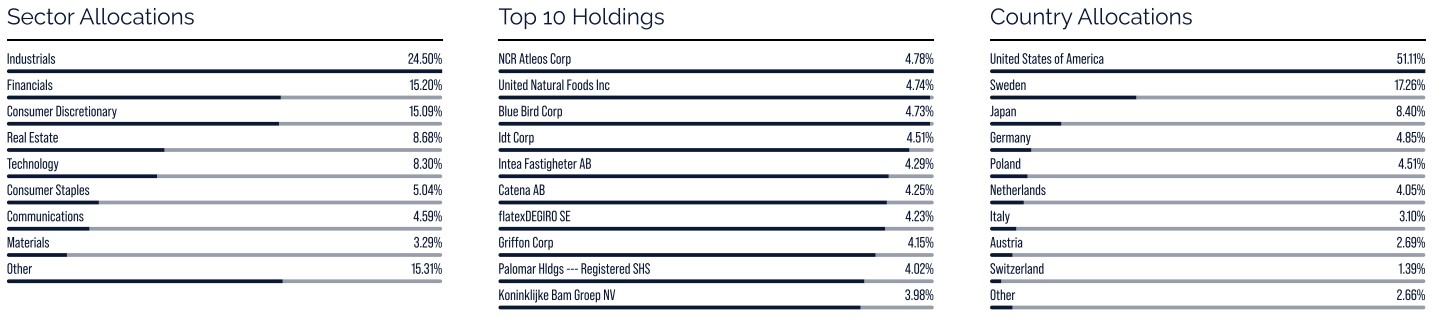

The strongest contributors to the fund's returns in March were United Natural Foods, Rusta, and United States Lime & Minerals, and the weakest were Griffon, Takasago Thermal Engineering, and Catena.

Unfortunately, this was another month in which geopolitical events dominated. The conflict in the Middle East, which had a massive impact on the flow of oil and other key inputs, created uncertainty in the global economy. Inflation expectations rose, as did market interest rates, postponing the cyclical recovery in both Europe and the US that we had positioned the fund for.

Among the fund's holdings, we have seen declines in cyclical industrials and construction, consumer discretionary, and other interest rate-sensitive stocks like real estate. Beyond company-specific news, this is also where we find the fund's poorest performers during March: Griffon, Takasago Thermal Engineering, and Catena. The fund's star performer, United Natural Foods, once again delivered a solid report and, as expected, lifted its expectations for the full year. Analysts have long been extremely negative about the company, despite its successful turnaround, but following this latest report, we have seen them change their minds, offering further fuel to the share's positive price movement.

Key market events and trends

Q1 2026 has now come to an end and we can say that it has been especially eventful in many ways. For one, US foreign policy has swung from one incitement to the next. The kidnapping of Venezuela's president, threats to forcibly occupy Greenland, and, finally, the attack with Israel that eliminated Iran's leadership. The subsequent conflict has impacted the global energy market, with the oil price shooting up 75% to more than USD 100 per barrel and interest rates rising in tandem. Given this, consumer sentiment remains weak and households around the world are building up savings buffers, although private consumption has risen modestly.

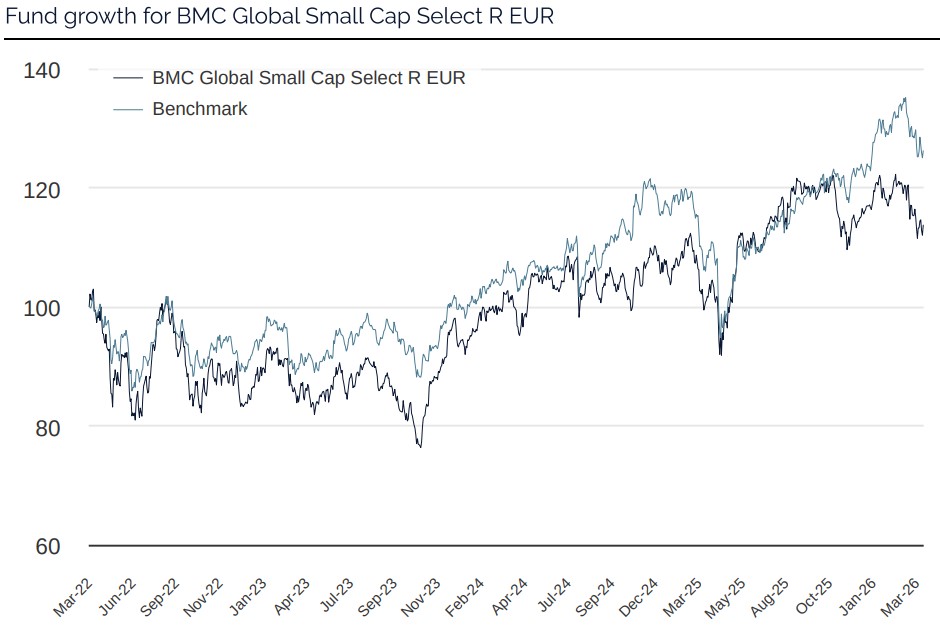

The equity markets shook off much of the initial impact and rose 5–8% in a widespread rotation from mega-cap tech stocks to the broader market. The Iran conflict brought this to a halt, and share prices have since fallen by some 10% from the peak, leaving the larger indexes at around -1% for the year so far.

Profit expectations for 2026 thus remain good, with consensus pointing at 19% growth, up strongly from the 14% that was forecast at the start of the year. Tech is the key driver, with energy stocks having also seen considerable upward profit estimate revisions. A subsector that stands out is semiconductors, where a handful of memory producers—Micron, Samsung, and SK Hynix—have together seen their 2026 profit forecasts doubling thanks to higher prices for traditional memory chips. Semiconductor capacity will soon catch up and prices for memory chips will normalize. This year, and possibly also next, look set to be exceptionally profitable, spurred by increased use of AI and the expansion of datacenters for the companies referred to as hyperscalers.

Portfolio changes

Owing to the geopolitical events in the Middle East, we have reduced our exposure to cyclical and other interest rate-sensitive companies. At the same time, we have also increased and bought into companies with solid balance sheets, robust pricing power, and exposure to structural growth trends. During March, we bought Everus Construction, Ingram Micro, Renew Holdings, and Wesco. We sold off Heijmans and Truecaller. Heijmans has been one of the fund's best investments since its inception. We bought into the company in spring 2024 at around EUR 20 per share and sold off our final shares at about EUR 90 each. It traded at just over five times its underlying cash flows owing to tight margins when we bought in and we sold it at closer to 15x underlying cash flows after a couple of years thanks to high growth and significant margin expansion. Truecaller, on the other hand, has been one of the fund's worst investments since its start. We sold off most of the holding after the investment case was proven incorrect with the company's Q3 2025 report. We sold off the remaining small position after further negative news from the company. In hindsight, we paid too high a multiple based on inflated market expectations and misjudged sustainability in the business model of its main revenue stream.

Below we offer short summaries of our new holdings.

Everus Construction: A US installation company, primarily operating in electricity, which benefits from the enormous investments in datacenters, transmission, and power transmission. The most observant will remember that in our previous newsletter, we wrote that we had sold Everus after the share price doubled since its separate listing in the fall of 2024. During the turbulence in March, when the share price dropped 20% from the earlier peak, we reassessed our decision and bought back into the share. We believe the company's growth outlook is undervalued by the market, while the type of contracts it signs allow it to pass cost increases on to end-customers.

Ingram Micro: One of the world's largest IT distributors. The company is well positioned to benefit from the increased demand for GPUs and AI infrastructure from large corporate customer and from the IT hardware upgrade cycle for small and medium-sized companies. Its business model generates stable cash flows and, since its listing in 2024, the company has rapidly reduced its debt and returned capital to shareholders via dividends and buybacks.

Renew Holdings: A British construction and engineering company that focuses on building and maintenance of critical infrastructure such as railroads, roads, energy, and water. Its business model is founded on long-term framework agreements, where it has great opportunities to pass cost increases on to end-customers. The capital-light business model offers high cash conversion and returns on invested capital. Thanks to a solid balance sheet that provides breathing space for complementary acquisitions, the company is expected to maintain its double-digit growth pace.

Wesco: The largest distributor of electrical, energy, and communication products and components in the US, with a share of 10–15% of a fragmented market. The distributor business model is appealing, given stable cash flows and contra-cyclical working capital needs. Wesco benefits from economies of scale and holds solid pricing power. It is strong in digitalization, AI, automation, and the expansion and upgrade of the electricity grid. Above all, we find its 20% exposure to datacenters attractive. This area grew by 50% during 2025.

The fund's positioning

Currently, the fund comprises 39 companies exposed to a range of sectors and geographies but selected for their own merits. We believe that a concentrated yet diversified, actively managed small cap fund focused on stockpicking should, over time, offer the prerequisites for great returns to unitholders.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

NCR Atelos

United Natural Foods

Blue Bird

IDT Corporation

Intea

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026