The stocks that contributed most positively to the fund's performance were ABB, flatexDEGIRO and Warsaw Stock Exchange. The companies that had the weakest performance during the month were SAP, Airtel Africa and GMO Payment Gateway.

Key market events and trends

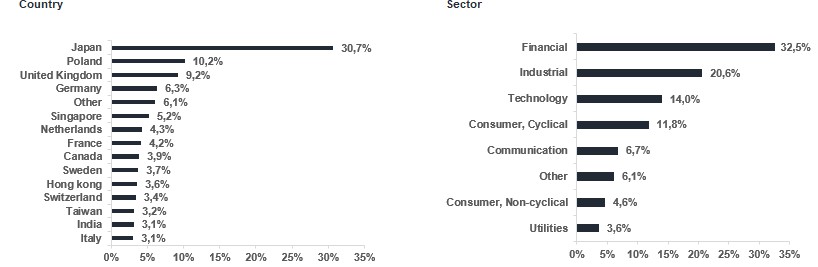

January was fairly stable in our focus markets of Japan, Poland and India. The Japanese snap election continues to attract attention, as the market tries to absorb and digest the economic promises announced by Japan's new Prime Minister. In addition, new and more aggressive reform measures targeting listed companies continue to emerge from Japan, which we view as very positive from a shareholder perspective.

Geopolitically, however, there was significant turbulence globally, including the kidnapping of Venezuela's president, the US threat of military action against Greenland, and unrest in both Iran and Minneapolis. Markets moved in the opposite direction though, with MSCI World rising 2.9% in USD, while the dollar weakened 1.4% against the EUR — an indication that investors currently view corporate earnings development in 2026 positively. The combined earnings forecasts currently stand at 10-14% growth.

Gold and silver experienced almost parabolic rises in early January, only to plummet when the new Federal Reserve chair was announced as Kevin Warsh. The rapid decline also unleashed a deleveraging in products exposed to gold and silver, which further exacerbated the drop. The markets see Kevin Warsh as a stabilizing force, minimizing demand for assets that are seen as safe havens.

The funds positioning

Below you can read about two of our holdings in the fund.

HDFC Bank

For the month, we had our Indian holding HDFC bank report very solid acceleration.

For those that don’t know HDFC, it is India’s largest bank and has very impressive financial return metrics. HDFC has benefitted significantly from India’s population starting their wealth generation journey, and regularly grew their loan book 15-20% generating significant wealth for shareholders.

Recently we have been given the opportunity to purchase HDFC at one of the cheapest prices in a decade. HDFC bank merged with HDFC ltd (their mortgage bank) and had to pause loan growth while deposit growth caught up. Their loan growth dropped from 15-20% to ~1.6%.

HDFC Banks Deposits have now caught up with loans and are guiding to 17% Loan growth this year, all while the bank is being priced for no growth, so we are looking forward to a “return to normal” for HDFC.

NEXT Plc:

In other news, our UK retailer NEXT Plc reported an incredibly strong trading update where they upgraded their earnings (again), reporting 8,8% growth in the UK (about 80% of their business) and +33% in International (about 20% of their business) for the 48 weeks to 27th December 2025.

NEXT Plc is an exceptionally well run clothing retailer which is expanding rapidly outside the UK, into Europe, the Middle East and eventually into the US etc. We see a very long growth runway for NEXT to possibly be the next H&M or Zara.

The other thing we like is the exceptional capital allocation that NEXT provides for shareholders. NEXT has consistently bought back shares (when they were cheap), while also paying out special dividends to shareholders from their excess capital. We received a special dividend this month from NEXT and look forward to their very shareholder friendly practices.

Amazingly, since January 2000, NEXT has returned 2085% return (not including dividends) vs. Microsoft with 731%.

Portfolio changes

During the month we purchased the Swedish company Sdiptech. Sdiptech is a serial acquirer that has historically acquired a number of lower quality companies. The company is now conducting a review of its portfolio and will gradually divest the weaker companies while retaining the quality ones. We believe this will have a positive effect on ROIC and it will become clear to investors just how well-run Sdiptech's high-quality companies truly are.

We are now entering an interesting earnings season where several of our holdings will communicate updated three-year plans, which often include a focus on higher margins, higher ROIC and share buybacks. These updated plans can often serve as strong catalysts for our holdings, and we look forward to sharing more about what is communicated in upcoming monthly letters.

Over time, our assessment is that a concentrated, yet diversified, actively managed global fund with a focus on exciting underlying markets and stock picking has the conditions to deliver strong returns to its unit holders.

We thank you for the trust in allowing us to manage your capital.

*MSCI ACWI ex USA NTR in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI ex USA Net Total Return USD Index In EUR, and is calculated according to the "high watermark" principle.

WARSAW STOCK EXCHANGE

Next

CANON MARKETING JAPAN

Kandenko

TMX Group

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026