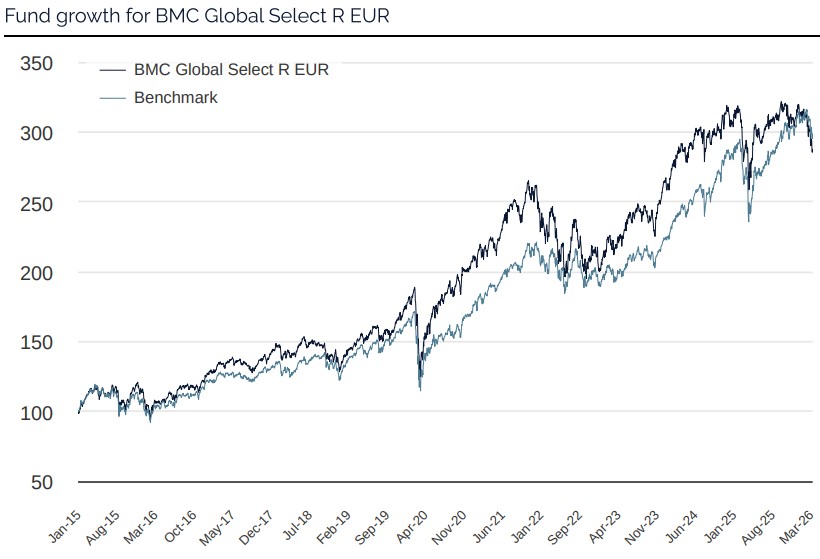

We note that our portfolio has been incorrectly positioned for the geopolitical challenges of the recent months. The fund does not hold any oil or gas companies (shares that have typically performed well during March) and has instead been positioned for further growth in cyclical investments such as US construction and European industrials (stocks that are experiencing headwinds owing to inflation/interest rate increases), as well as India (a country that imports much oil), and luxury consumer shares (where there are limited purchases of Hermes bags in Dubai right now). As a result, the fund's return was down 7.7% during March, coming in 2.6 percentage points worse than the fund's benchmark index*.

Based on share price movements we have seen following reports of a relatively positive outcome for the Iran conflict, we can also conclude that this portfolio positioning will be right if/when the oil price drops once more or when the market starts pricing in an end to the conflict.

The strongest contributors to the fund's performance in March were United Natural Foods, Singapore Exchange, and Prysmian, while the weakest were Hermes, Schneider, and Wheaton. The trend in United Natural Foods is particularly interesting given the positive improvements in the company, including cost savings, paying down of debt, and the positioning for growth, which has again and again surpassed market expectations. These internal changes are so significant that even the impact of this turbulent macro environment pales in comparison with all the positive moves the company is making. We aim to find more investments like this with these characteristics.

Key market events and trends

Q1 2026 has now come to an end and we can say that it has been especially eventful in many ways. For one, US foreign policy has swung from one incitement to the next. The kidnapping of Venezuela's president, threats to forcibly occupy Greenland, and, finally, the attack with Israel that eliminated Iran's leadership. The subsequent conflict has impacted the global energy market, with the oil price shooting up 75% to more than USD 100 per barrel and interest rates rising in tandem. Given this, consumer sentiment remains weak and households around the world are building up savings buffers, although private consumption has risen modestly.

The equity markets shook off much of the initial impact and rose 5–8% in a widespread rotation from mega-cap tech stocks to the broader market. The Iran conflict brought this to a halt, and share prices have since fallen by some 10% from the peak, leaving the larger indexes at around -1% for the year so far.

Profit expectations for 2026 thus remain good, with consensus pointing at 19% growth, up strongly from the 14% that was forecast at the start of the year. Tech is the key driver, with energy stocks having also seen considerable upward profit estimate revisions. A subsector that stands out is semiconductors, where a handful of memory producers—Micron, Samsung, and SK Hynix—have together seen their 2026 profit forecasts doubling thanks to higher prices for traditional memory chips. Semiconductor capacity will soon catch up and prices for memory chips will normalize. This year, and possibly also next, look set to be exceptionally profitable, spurred by increased use of AI and the expansion of datacenters for the companies referred to as hyperscalers.

Portfolio changes

We made some exciting changes to the fund during the month, further refining our focus on finding companies with substantial internal improvement potential. We have increased in construction-related holdings in response to the ongoing energy transition around the world, buying Italy's Prysmian, the US's Everus Construction, and BAM Group from the Netherlands. The companies have shown solid growth through improved margins when signing new contracts at higher margins than those that have run their course, and all three look set to make value-creating acquisitions in the next six months that should drive their share prices higher. To finance these investments, we sold two Special Situations: Singapore's SEA, which we had bought at too high a valuation; and the US's Charles Schwab, which proved a successful investment, with the share price hitting our target. We also made a change in the Asian portion of the fund and, after meeting the company in Tokyo, we invested in Coca-Cola Japan. Having not raised its prices for around 30 years, the company has now started to use its pricing power, and this, together with cost savings, is swelling its profits considerably. In other words, there are many positive internal improvements in the company—just as we like it.

The fund's positioning

The fund now comprises 35 companies across a range of sectors and geographies but chosen on their own merits. What stands out in the portfolio right now is just how cheap many of the world's leading companies are. Several, such as Microsoft, Amazon, and Mastercard, we haven't seen this cheap except in times of major crisis. This leaves us feeling particularly optimistic for the rest of the year, and we anticipate a generally robust equity market if/when the Iran conflict ends.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

Amazon

TSMC

MASTERCARD INC

Vulcan Materials

MICROSOFT CORP

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026