The strongest contributors to the fund's development in May were Mediatek, AMD, and SK Hynix, while the weakest were Arista Networks, Fujikura, and NU Holdings.

The upward trend among tech stocks that we saw in April continued during May, which proved another strong month for the fund. This was as a result of the low valuations we saw at the end of March and the increased optimism for AI-related companies. For example, during May, Anthropic reported annual revenues now at a massive USD 47bn, up from USD 30bn just a month before. This means that Anthropic has increased its revenues by an amount representing all of Atlas Copco's in just one month.

The month of May saw reporting season continue, and a majority of the fund's companies have now reported. Our overall conclusion is for ongoing solid profit growth and estimates for most companies being lifted. When Nvidia released its report, it was yet another in a series of strong results. The company again beat estimates, with revenues growing by 85% y/y. The biggest talking point was Jensen Huang's comments regarding the enormous rise in demand for CPUs, rather than the GPUs that are the current cash cow. The company's guidance is for the entire CPU market to increase to USD 200bn, which is almost twice as high as the earlier announcements of USD 120bn from AMD and ARM. Only a few days before, AMD had raised its expectations from USD 60bn. This benefits the fund's CPU-related companies—Intel, AMD, and ARM—which saw their share prices increasingly immensely during May.

Broadcom also reported robust numbers, with profit growth of 54%, and with guidance of doubling its AI chip revenues to USD 100bn next year. Hardly a weak report in our eyes, but its share traded down 12% on the report as it did not beat estimates more. We believe this growth is limited in the short term by the availability of manufacturing capacity. An undeniably strong report, but one for which expectations played a role. We remain positive on the ASIC trend that benefits Broadcom and Mediatek most of all, and not least Alphabet, which recently announced a capital increase of almost USD 85bn, of which we believe a considerable sum will be spent on these two companies.

In addition to Alphabet, new capital will also flow into the AI market given the some USD 150bn expected in conjunction with the listings of SpaceX, Anthropic, and OpenAI later this year. SpaceX will list first, on 12 June.

During May, we undertook an exciting analysis trip to Hong Kong and Shanghai. A video of our thoughts about the trip and the latest trends we saw can be found on our website. A couple of inspiring blog posts will be published soon, too.

Key market events and trends

A 5% rise in the MSCI World (EUR) during May disproved the old saying "sell in May and go away." The return profile for 2026 tells a story of a constantly evolving market after the year started with a marked increase in gold and silver, along with a clear rotation out of the software sector, followed by a rise in oil and gas when the Iran conflict dominated the headlines in March. As the tension eased, AI infrastructure, memory chips, and semiconductors in particular took the lead from April. AI is, without a doubt, the strongest driver of the market right now. Data centers are being built at an incredible pace, especially in the US, but the trend is spreading to Europe, China, India, and other large economies. We see more and more AI-powered products and services in everyday life, leaving us in no doubt that this technology is here to stay.

Fundamentals continue to strengthen globally. At the start of 2026, the market had expected profit growth for MSCI World of around 14% for the full year. This has since been revised up to 20%, with expected growth of 14% for 2027. Even though the market is currently trading at an all-time high, valuations for 2027 profits remain moderate at a P/E of 16.5x.

Finally, Europe is changing at a rapid pace that may not yet be fully reflected in the region's market valuations. SoftBank's announced investment of EUR 75bn in a data center in France is a recent example. More broadly speaking, the emerging alliance between the "Democratic Seven"—the EU, Australia, New Zealand, Japan, South Korea, Canada, and the UK—represents a structural shift that the stock market has not yet fully priced in.

Portfolio changes

During May, we bought into three new holdings: Silex Microsystems, Taiwan Union Technology, and Charles Schwab. And we exited Silex Microsystems, Visa, and Uber.

We bought into Silex Microsystems during its listing and sold the shares the same month. It's an appealing company with [KT1.1]good prospects, but as its valuation propelled upwards, we chose to sell.

The fund's positioning

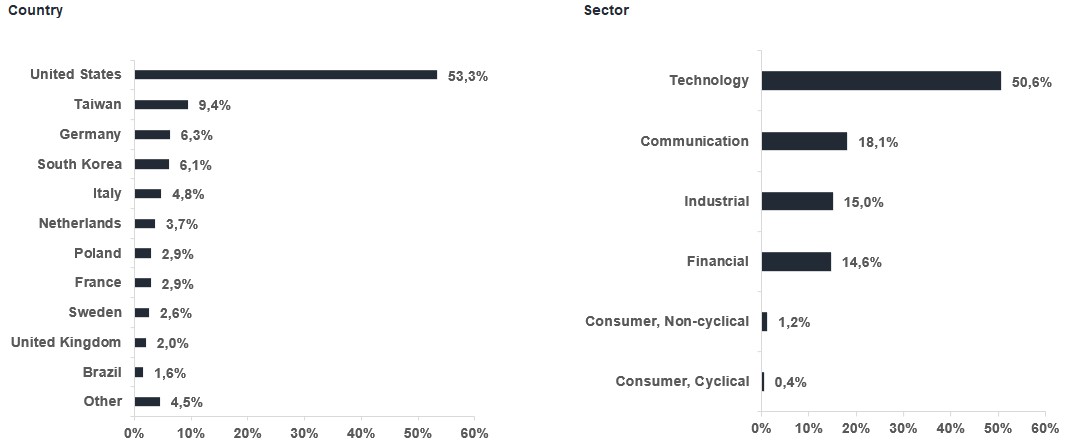

The fund now comprises 42 companies exposed to a range of sectors and geographies, with companies chosen on their own merits. We do not limit ourselves only to tech stocks but invest in companies across sectors exposed to technology. The portfolio as a whole maintains high forecasted profit growth of 27% for next year. We believe a concentrated but also diversified, actively managed small cap fund focused on stockpicking has all the prerequisites to deliver great returns to its unitholders over time.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

AMD

Mediatek

ALPHABET

MICROSOFT CORP

Broadcom

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 11 jun 2026

Monthly Newsletter | 11 jun 2026

Monthly Newsletter | 11 jun 2026