The strongest contributors to the fund's return in May were Covenant Logistics, BAM Group, and First Advantage, while the weakest were Palomar, Limbach, and Kandenko.

The most stellar contributor, Covenant Logistics, a US logistics solutions provider, has, like its competitors, benefited from the massive increase in freight rates in the US this year. Following more than 40 months of freight rate recession—the longest in modern history—the end of 2025 saw significant structural changes in the industry. The Trump administration's more stringent regulations for drivers, such as stricter certification and English language proficiency requirements, led to a shortage (the industry judges that as much as 10% of all freight drivers in the US have lost their right to drive trucks). The shortage of drivers has increasingly tightened the supply of trucking services, coinciding with a strengthening of the industrial sector, which has rapidly driven freight rates up to new record levels. For Covenant Logistics, this should lead to accelerating growth and markedly higher margins during the second half of 2026 and, more importantly, during 2027, as customer contracts are renewed based on the prevailing market conditions.

The weakest contributor during the month was Palomar. The company delivered a solid quarterly report in early May, with 23% growth in adjusted earnings, an adjusted ROE of 27%, and higher guidance for full-year 2026. Despite this strong report, the share price dropped on negative sentiment around the US insurance industry, which, after several years of steady price increases, has normalized and even seen prices decline in some areas. Palomar is an especially niche insurance company, with ~90% of its revenues unaffected by price developments in the wider industry, something that can be seen in the company's consistently solid results despite slowdowns in the sector. Palomar now trades at ~10x its guidance for 2026 profits, which we believe implies attractive risk/reward for one of the industry's best-run companies, offering great opportunities for ongoing profit growth in the coming years.

Key market events and trends

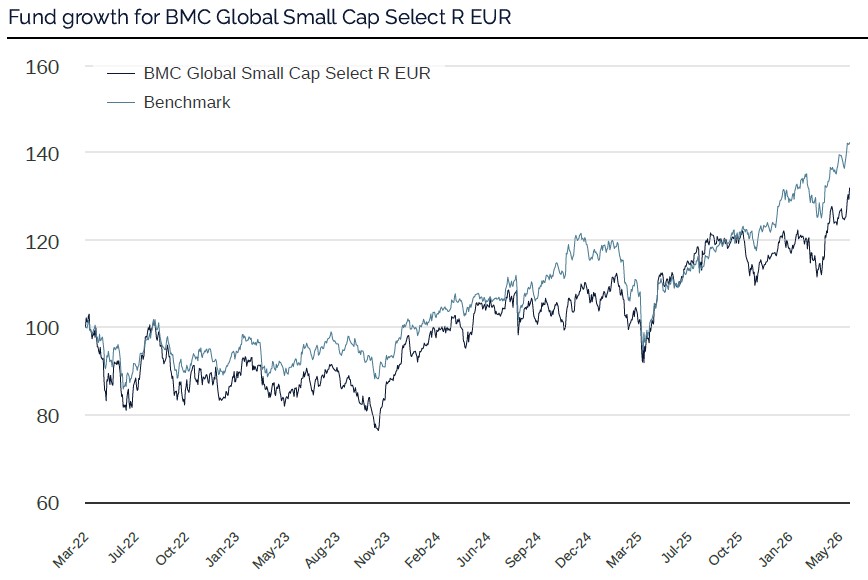

A 5% rise in the MSCI World (EUR) during May disproved the old saying "sell in May and go away." The return profile for 2026 tells a story of a constantly evolving market after the year started with a marked increase in gold and silver, along with a clear rotation out of the software sector, followed by a rise in oil and gas when the Iran conflict dominated the headlines in March. As the tension eased, AI infrastructure, memory chips, and semiconductors in particular took the lead from April. AI is, without a doubt, the strongest driver of the market right now. Data centers are being built at an incredible pace, especially in the US, but the trend is spreading to Europe, China, India, and other large economies. We see more and more AI-powered products and services in everyday life, leaving us in no doubt that this technology is here to stay.

Fundamentals continue to strengthen globally. At the start of 2026, the market had expected profit growth for MSCI World of around 14% for the full year. This has since been revised up to 20%, with expected growth of 14% for 2027. Even though the market is currently trading at an all-time high, valuations for 2027 profits remain moderate at a P/E of 16.5x.

Finally, Europe is changing at a rapid pace that may not yet be fully reflected in the region's market valuations. SoftBank's announced investment of EUR 75bn in a data center in France is a recent example. More broadly speaking, the emerging alliance between the "Democratic Seven"—the EU, Australia, New Zealand, Japan, South Korea, Canada, and the UK—represents a structural shift that the stock market has not yet fully priced in.

Portfolio changes

During May, we added a new holding and also exited a Special Situations stock that had reached the target we had set for it. We also sold off some smaller positions that we judged were now fully valued after a great share price development. The companies we exited were BlueBird, Note, Revo Insurance, and Rusta.

BlueBird is an interesting one to highlight as an example of a company that has undergone a positive change that the market finally took notice of. We wrote more about this in this blog post in August 2024. Recently, the company reached a more reasonable valuation, and we also spotted a change in the order book's mix. The share of electric buses, representing around three times higher order value per unit and higher margins than diesel buses, narrowed as a share of the total, owing to the Trump administration cutting back on subsidies for electric buses. Meanwhile, as order volumes, measured as the number of buses, are largely constant y/y, there is a risk of both lower revenues and some margin pressure in the future.

The company we took a stake in was Sinch. This is the world's largest digital communications firm. Sinch provides infrastructure that enables effective customer communication via messaging, voice, and email. Following a period of aggressive, acquisition-driven expansion, the new management team has focused on integration, improved profitability, and disciplined capital allocation, including significant share buybacks. The company's growth in recent years has been hindered by external factors such as a weaker market and negative currency effects, as well as internal measures such as the elimination of low-quality revenues. Given better market prospects, including rising AI usage, and the completion of the integration work, growth should accelerate during the second half of the year, while there are also opportunities to expand margins to the upper end of—or even beyond—the company's target range.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

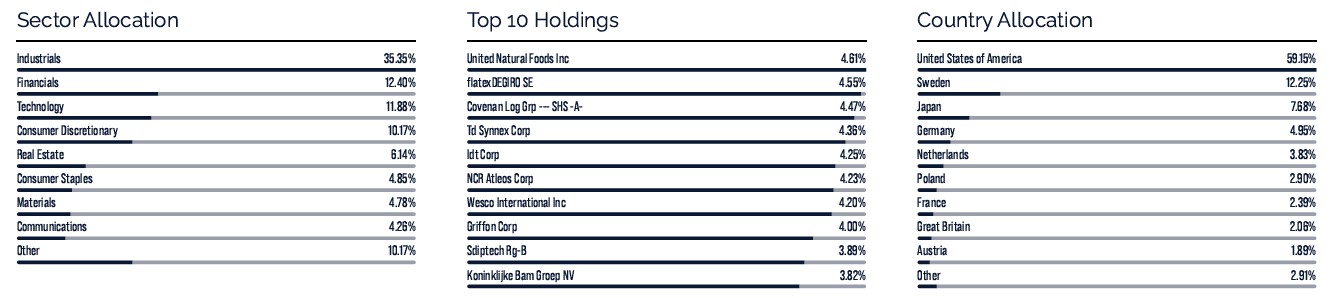

United Natural Foods

flatexDEGIRO

Covenant Logistics

TD Synnex

IDT Corporation

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 11 jun 2026

Monthly Newsletter | 11 jun 2026

Monthly Newsletter | 11 jun 2026