The strongest contributors to the fund's returns during the month were Deutsche Boerse, ARM, and Prysmian, while the weakest were Schneider Electric, Mediatek, and Warsaw Stock Exchange.

The month of March again saw chaotic equity markets, primarily impacted by the conflict between the US and Iran. Uncertainty prompted the oil price to rise, increasing by almost 80% since the start of the year, and the markets hit the sell button. A number of the statements from Trump since the start of the conflict had the markets swerving between hope and doubt on an almost daily basis, prompting both sizable declines and rallies in stock prices. The VIX index of expected volatility reacted by touching its highest level since Trump's tariff moves last April. We note that at these levels of VIX in the past, there have been among the best long-term buying opportunities in the equity market.

Also, valuations in general, but primarily in tech, have been especially attractive since the start of the conflict with Iran. For example, Microsoft currently trades at a P/E of 19x (five-year average of 28x) and Nvidia at a P/E of 16x (five-year average of 34x). The equivalent valuation for Telia is, at the time of writing, at 19x, which is telling for how cheap valuations have become. We have become more convinced in recent weeks that we are nearing the valuation trough for tech stocks and that peace in the Middle East would most likely get share prices moving again.

We have again seen signs of encouraging development in AI during March. TSMC reported 30% y/y growth for February, while Anthropic (the company behind AI model Claude) announced it had reached USD 300bn in ARR, which is three times the level it ended 2025 at. This incredible growth drives demand for semiconductors and has created a considerable deficit in the value chain, something we discuss in our latest blog post about our analyst trip to Japan and Taiwan, during which we met more than 20 companies (click here to see the film). Several companies in the portfolio benefit from this, including ASML, Samsung, SK Hynix, and Fujikura.

Key market events and trends

Q1 2026 has now come to an end and we can say that it has been especially eventful in many ways. For one, US foreign policy has swung from one incitement to the next. The kidnapping of Venezuela's president, threats to forcibly occupy Greenland, and, finally, the attack with Israel that eliminated Iran's leadership. The subsequent conflict has impacted the global energy market, with the oil price shooting up 75% to more than USD 100 per barrel and interest rates rising in tandem. Given this, consumer sentiment remains weak and households around the world are building up savings buffers, although private consumption has risen modestly.

The equity markets shook off much of the initial impact and rose 5–8% in a widespread rotation from mega-cap tech stocks to the broader market. The Iran conflict brought this to a halt, and share prices have since fallen by some 10% from the peak, leaving the larger indexes at around -1% for the year so far.

Profit expectations for 2026 thus remain good, with consensus pointing at 19% growth, up strongly from the 14% that was forecast at the start of the year. Tech is the key driver, with energy stocks having also seen considerable upward profit estimate revisions. A subsector that stands out is semiconductors, where a handful of memory producers—Micron, Samsung, and SK Hynix—have together seen their 2026 profit forecasts doubling thanks to higher prices for traditional memory chips. Semiconductor capacity will soon catch up and prices for memory chips will normalize. This year, and possibly also next, look set to be exceptionally profitable, spurred by increased use of AI and the expansion of datacenters for the companies referred to as hyperscalers.

Portfolio changes

During March, we sold two holdings and bought into five more. We sold SEA and SAP, and we added Prysmian, Fujikura, ASML, Samsung Electronics, and Tokyo Electron to the fund.

Prysmian and Fujikura are both active in fiberoptic cables for datacenters, an area where there is currently a severe shortage, causing prices to rise sharply. This stems from all the datacenters being built where the network equipment is being switched from copper to fiber cables to increase the speed, quantity, and distance over which data can be transported. We anticipate a solid structural trend for fiberoptics in the coming years.

ASML is Europe's leading tech company, holding a monopoly on the EUV machines necessary to produce semiconductors. TSMC is a key customer that is now increasing its investments significantly to meet the growing demand for AI chips, which benefits ASML. We see potential for double-digit growth for some years to come.

On the same theme, we have also invested in Tokyo Electron, which is a Japanese machine manufacturer for semiconductors and an industry peer to ASML. The company offers a broad range of machines used in several stages of production. Its profits are expected to grow by just over 20% a year over the next two years.

Samsung is a new Special Situations stock operating in memory chips. The company has a robust position in the manufacturing of DRAMs and is now starting to compete to a greater extent within HBM (high bandwidth memory), which is used in AI chips. The supply of memory chips will remain limited in the coming years, implying that prices should remain high. The company's expected total profits for the next three years are equivalent to half its market cap. The share trades at just over 6x P/E for next year, which we consider a particularly appealing valuation.

The fund's positioning

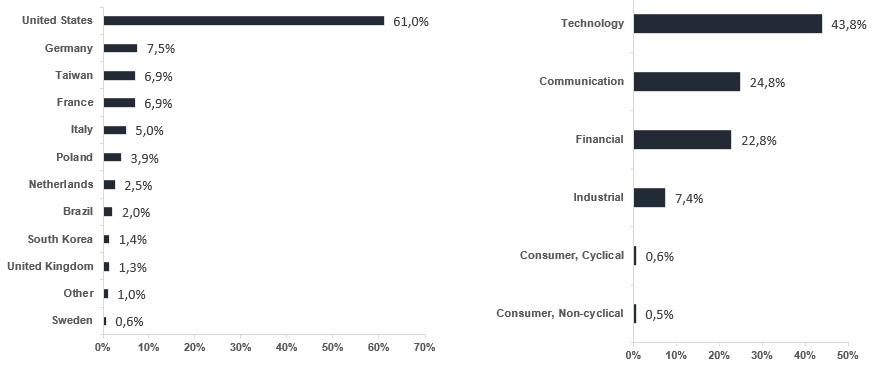

As of now, the fund comprises 39 companies across a range of sectors, geographies, and drivers, but which are selected on their own merits. The total portfolio remains at a high profit growth forecast of 27% for next year. Our fund is also very appealingly valued at a P/E of 20x, which represents a PEG ratio (valuation in relation to profit growth) of less than 1x. We believe that a concentrated but also diversified, actively managed global technology fund that focuses on stock picking has the characteristics to deliver great returns to unitholders over time.

*MSCI AC World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

Amazon

MICROSOFT CORP

ALPHABET

NVIDIA CORP

APPLE

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026