The strongest contributors to the fund’s performance for the month were Arista Networks, AMD, and flatexDEGIRO, while the weakest were Intuit, Salesforce, and SAP.

January was a month of robust share price movements for semiconductor companies, with the increasingly tight supply chain to meet the still strong demand for computing power. TSMC’s report acted like a rocket when the company both raised its growth guidance to 25% a year through 2029 and announced an investment of more than USD 150bn in capex to expand its manufacturing capacity in the coming years. The market reacted positively in appreciation of the company’s clear signals regarding the ongoing strength in demand. On the other hand, the software companies are still plagued by the historically weak sentiment seen at the end of last year. This worsened in mid-January when Anthropic launched Claude Cowork, prompting the market to severely question the future existence of software companies. Claude Cowork can be described as a more user-friendly version of Claude Code, which is primarily aimed at professional software developers. Just as ChatGPT placed AI models into the hands of the average user, Anthropic can now be said to have done the same with an AI agent that can program software using human language rather than complicated code. The barriers to program software can rapidly be dismantled, with the democratization of software development as a result. This strengthens our belief that the future of software development lies with those companies that are hard to disrupt with AI—access to unique customer data is crucial.

The launch of Claude Cowork takes us one step closer to a world where AI agents can truly be of benefit to the general public. We believe the software industry will change but not disappear. Many companies will be affected, turning more effective in the coming years. This will sort the wheat from the chaff, as we saw with Google last year. AI has clearly shown that yesterday’s winners can quickly become today’s losers (and vice versa), something that speaks to active investment management. We remain fascinated by these breakthroughs in the AI market and the changes they render. Changes we can capitalize on in this fund.

During January, a couple of companies reported, including Meta, which released solid numbers and guidance implying that its extensive investments are starting to bear fruit; the share price rose 10% in response. Microsoft and SAP both traded down considerably on their reports, despite the solid underlying figures.

Key market events and trends

January 2026 proved one of the most geopolitically turbulent starts to a year for a long time, with the kidnapping of Venezuela’s president, the US’s threat of military action in Greenland, and unrest in both Iran and Minneapolis.

The market moved in the opposite direction, however, with MSCI World increasing by 2.9% in dollar terms, while the dollar itself weakened by 1.4% against the euro—an indication that investors are currently positive regarding companies’ earnings outlooks for 2026. The weighted earnings forecast is for 10–14% growth, with US tech companies standing out at expected +27% growth. Company reports in January supported these expectations to an extent, although market reactions in individual stocks, such as Microsoft and SAP, were unexpectedly volatile versus what the companies actually delivered.

Gold and silver experienced almost parabolic rises in early January, only to plummet when the new Federal Reserve chair was announced as Kevin Warsh. The rapid decline also unleashed a deleveraging in products exposed to gold and silver, which further exacerbated the drop. The markets see Kevin Warsh as a stabilizing force, minimizing demand for assets that are seen as safe havens.

In February, we await a wave of company reports that will also include 2026 guidance. Indications suggest stable profit growth.

Portfolio changes

We did not sell any holdings during January, but we bought into two new companies. At the beginning of the month, we took a position in REVO Insurance, an exciting Italian company offering insurance for small and medium-sized businesses. REVO has developed its own technology to price insurance and handle claims, allowing it to offer policies faster, more effectively, and at the correct price and risk levels. This is a great example of a company that, thanks to its proprietary tech, can grow by around 20% a year and take market share from larger competitors. REVO is attractively valued in relation to its growth and is now expanding into Spain. The company’s management, CEO, and founder own 16%.

During the month, we also took a position in Sweden’s Lime Technologies, a company founded in Lund that builds niche CRM systems largely for energy and real estate companies in northern Europe. Lime has undergone a period of lower growth owing to a weaker market and a cyberattack last year, but these are now in the past. We anticipate stronger growth, with the company now trading at an appealing FCF yield of 4.5%.

The fund’s positioning

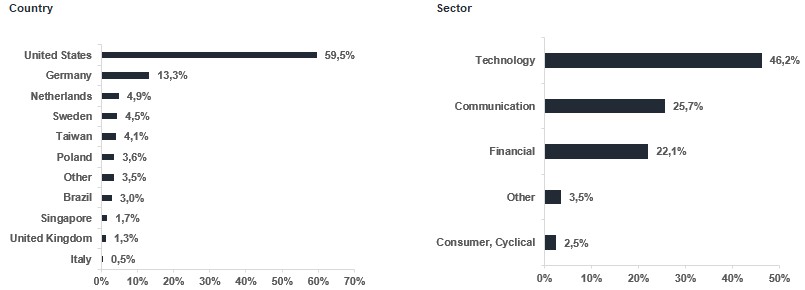

The fund now comprises 37 companies exposed to a range of sectors, geographies, and business drivers, with each company chosen on its own merits. Overall, the portfolio maintains high expected profit growth of 22% for next year. We consider the fund appealingly valued at a PEG ratio (valuation in relation to profit growth) of around 1x. We believe that a concentrated but also diversified actively managed global technology fund that focuses on stock picking has the characteristics to deliver great returns to unit-holders over time.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

NVIDIA CORP

MICROSOFT CORP

Analog Devices

Arista Networks

TSMC

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026