The shares that contributed the most during the month were Blue Bird, VBG Group, and Lindex Group. Those with the weakest performance were Enghouse Systems, Alamo Group, and Eagle Materials. The month’s best share was the US’s Blue Bird, up around 30% on its reporting day. The share saw a massive leap when earnings per share beat expectations by 89%. The company lifted guidance for both revenues and EBITDA.

In May, our global team attended the capital markets days for Munters and Fortnox. Munters holds a solid position in refrigeration equipment for battery plants and data centers. It announced an increased focus on more advanced systems, with the sale of some areas of its Food Tech business where systems are simpler. Fortnox is the leader in corporate services for small and medium-sized enterprises. It offers an ecosystem of services, such as accounting, payroll, and invoicing. The company, which hosted an excellent CMD, is skilled at running its businesses with good growth, high profitability, and extensive innovation.

We’d also like to remind you that our firm has now changed name to Brock Milton Capital, with our global small cap fund changing name to BMC Global Small Cap Select.

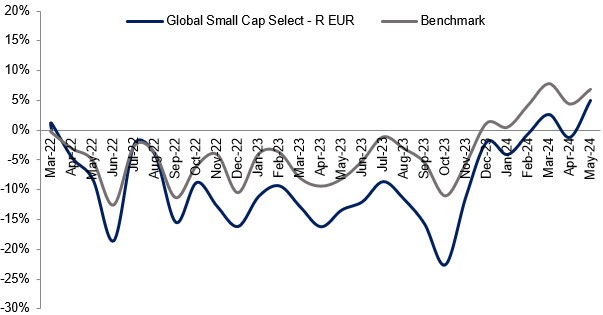

Key market events and trends (what has influenced performance most?)

For once, Sweden’s Riksbank was among the first to cut key interest rates, with the ECB following suit a few weeks later. One of the market’s major considerations now is when the Fed will do the same as its European central banking colleagues.

There’s a bit of a battle going on to take price levels down further to a sustainable level so that we can finally see the long-awaited interest rate cuts. That both the S&P 500 and NASDAQ are currently trading at all-time highs suggests that investors have already priced in interest rate cuts to some extent. Such investor confidence in the equity markets is positive. If we were to raise one concern it would be that the difference between the S&P 500’s profit margin (EPS/index price) and the yield on US 10-year treasury bonds is too narrow. At current interest rates, bonds are still all too appealing an alternative for investors. Some years ago, we discussed TINA (There Is No Alternative), but now it is bonds that are the interesting investment alternative.

Portfolio changes

During May, we bought three new companies and sold four to increase the opportunities for good returns for unitholders. In last month’s newsletter, we said we had been compelled to sell our Polish holdings, Text and Autopartner, because of fund mergers. As this is now completed, we bought back these two interesting Polish holdings. We also added an exciting Dutch Special Situations holding. We believe construction company Heijman can double its share price in the next two to three years through a combination of low valuation and increasing profits.

We sold US security company Napco Securities, Dutch energy tech company Alfen, US construction firm Sterling Infrastructure, and Italian HVAC company Carel Industries.

The fund’s positioning—our market expectations

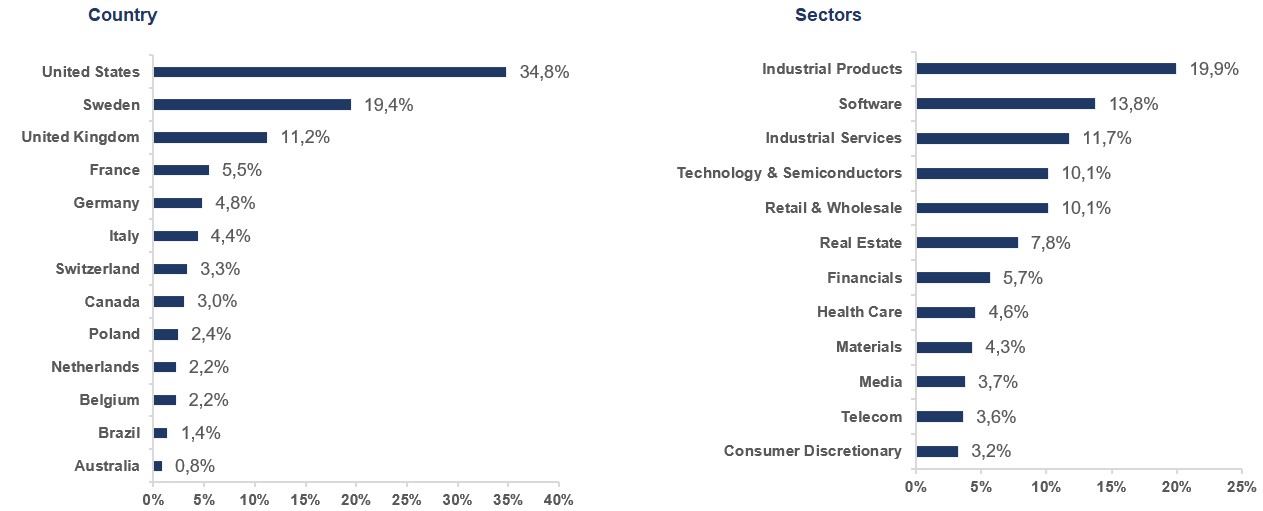

We see considerable upside in small caps relative to larger companies, as the asset class will benefit from a lower policy and market interest rate environment. The estimated profit growth in our global small cap fund is around 17.3% y/y, with a P/E valuation of 17.8x for next year. This implies a PEG ratio of 1, which highlights the attractive valuation of small caps. Ahead, we expect the share prices to be driven by, among other things, analysts lifting target prices owing to higher profit forecasts for 2025 as the economies start to grow again.

We thank you for your continued faith in us in investing your capital.

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

Blue Bird

VBG GROUP

Exclusive Networks

IDT Corporation

Legacy Housing

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026