The stocks contributing the most during the month were Heijmans, Exclusive Networks, and Legacy Housing. Those with the weakest performance during July were Axcelis Technologies, Pluxee, and Lindex Group.

The Netherlands' Heijmans offered a decent contribution to the fund's returns thanks to a solid report, with turnover up 30% and raised guidance for the EBITDA margin. Instalco of Sweden also contributed well, as the market began to discount increased construction sector activity owing to a lower expected interest rate level. Several companies will release their quarterly reports in August, and we look forward to discussing these in our next newsletter.

Key market events and trends (what has influenced performance most?)

The market events that had the greatest stock market impact during the month were a general tech frenzy, particular concern about semiconductors, and general uncertainty about a deteriorating US economy. Beyond that, there has also been the further negative developments in the conflict between Israel and Hamas/Hezbollah/Iran, which have cast a wet blanket over the market. After the turn of the month, we have also seen a sharp downturn in the Japanese equity market, affecting global exchanges, with large drops as a result. When the Japanese central bank somewhat unexpectedly decided to raise interest rates, the enormous Yen carry trade forced many hedge funds to unwind their positions, leading to large market movements. These movements will probably diminish quite quickly once the positions are sold. We do not own any Japanese companies in the fund.

The market also reacted to the failure of investments by larger tech firms (software and semiconductors) in Artificial Intelligence (AI) to deliver sufficiently rapid increases in turnover and profit to match market expectations. In addition, the US has announced a much tougher stance on exporting "high tech" and western-produced semiconductors to Chinese tech companies, which has hurt companies in that industry. And when it comes to the US economy, labor market data was worse than expected. On the one hand, the equity market wants "worse" unemployment figures so that there is no doubt that the Fed will cut interest rates in September. But, on the other, the figures shouldn't be so bad that the US heads into recession and negative growth. Right now, the fixed income market is pricing in that the policy rate can be as much as 1.5 percentage points lower at year-end than it is today.

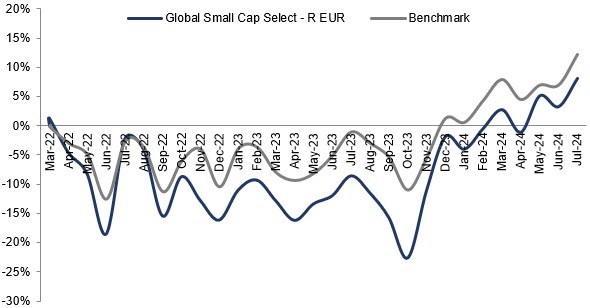

Small caps had their best period in a long time in July, supported by central bank communications about lower policy rates. During July, MSCI's global small cap index did nearly five percentage points better than the "big" index of the world's largest listed companies. We have finally begun to see the stock price movements in small caps that we have been awaiting for more than a year.

Portfolio changes

During July, we sold the UK's YouGov after the company posted a profit warning. We added no new holdings to the fund.

The fund's positioning—our market expectations

Forecasted profit growth for the companies in our small cap fund has risen by some 20% y/y, with a P/E valuation of just below 15x on next year's profits. This implies a PEG ratio of less than 1, highlighting the particularly attractive valuation of our small cap fund. We note that profit estimates have risen by around three percentage points from the previous month's summarized forecasts. We believe the rising profit estimates can prove a key stock price driver for the holdings in our global fund.

We thank you for your continued faith in us in investing your capital.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

Legacy Housing

Exclusive Networks

Siegfried

REV Group

Covenant Logistics

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026