The best contributors to the fund’s performance in the month were Patrick Industries, United Natural Foods, and Climb Global, while the weakest were IIFL Finance, Palomar, and First Advantage.

Despite the reasonably large market movements in January, there was little company-specific news to explain the individual increases and decreases in the fund’s holdings. Patrick Industries, which was the strongest contributor in January, saw its share price rise by almost 20% at the start of the year, despite a lack of company-specific factors. The company is a US manufacturer of particular exterior and interior products for motorhomes, boats, and small houses. After several years with weak demand from end-customers and retailers’ inventories at record-lows, several of the company’s markets have now troughed and we anticipate that smaller increases in demand from end-customers can now have a greater effect on Patrick Industries’ production volumes when retailers need to expand inventories again. It is possible that the market will begin pricing in that this is imminent, given lower interest rates and large tax refunds in the US.

Conversely, we have seen a lot more news from IIFL Finance, which was the weakest contributor to the fund’s January performance. The company delivered a solid quarterly report with the total loan book growing by 38% y/y, primarily driven by gold loans, while the net interest margin improved and profits surpassed market expectations. Unfortunately, in conjunction with the report, it also reported that the Indian tax authorities have decided to undertake a deeper audit of the company. This is nothing unusual and often occurs with more complex companies. However, the audit implies increased risk, potentially casting a wet blanket over the share price while it is ongoing. We thus chose to sell down our position in the holding while we await the audit results.

Key market events and trends

January 2026 proved one of the most geopolitically turbulent starts to a year for a long time, with the kidnapping of Venezuela’s president, the US’s threat of military action in Greenland, and unrest in both Iran and Minneapolis.

The market moved in the opposite direction, however, with MSCI World increasing by 2.9% in dollar terms, while the dollar itself weakened by 1.4% against the euro—an indication that investors are currently positive regarding companies’ earnings outlooks for 2026. The weighted earnings forecast is for 10–14% growth, with US tech companies standing out at expected +27% growth. Company reports in January supported these expectations to an extent, although market reactions in individual stocks, such as Microsoft and SAP, were unexpectedly volatile versus what the companies actually delivered.

Gold and silver experienced almost parabolic rises in early January, only to plummet when the new Federal Reserve chair was announced as Kevin Warsh. The rapid decline also unleashed a deleveraging in products exposed to gold and silver, which further exacerbated the drop. The markets see Kevin Warsh as a stabilizing force, minimizing demand for assets that are seen as safe havens.

In February, we await a wave of company reports that will also include 2026 guidance. Indications suggest stable profit growth.

Portfolio changes

During January, we sold off three holdings. We exited Lindex Group as the company’s streamlining and expected consequent upward revaluation was dragging on and as it was finding it hard to identify an acquirer for its loss-making Finnish department store. Nordnet is a particularly well-run company but one we believe is now fully valued following its strong share price run. We thus see better returns potential elsewhere. Tutor Perini has seen a solid performance since we bought in almost a year ago. This is what we wrote about the company in March 2025:

Tutor Perini is a US construction company focused on large-scale infrastructure projects and complex buildings. Its order book is nearly five times its turnover, leaving it expecting robust profit growth for the coming years. In only a short time, it has gone from high indebtedness to almost sitting on net cash. This, combined with solid cash flows, means we expect large share buybacks in the future.

The company has executed on its solid order book and consistently raised profit guidance during the year while its cash conversion has also been stellar. It has turned net debt into net cash and initiated programs for both buy-backs and dividends. We are happy with the share’s almost 200% price increase and now see better risk-adjusted returns potential elsewhere.

The fund’s positioning

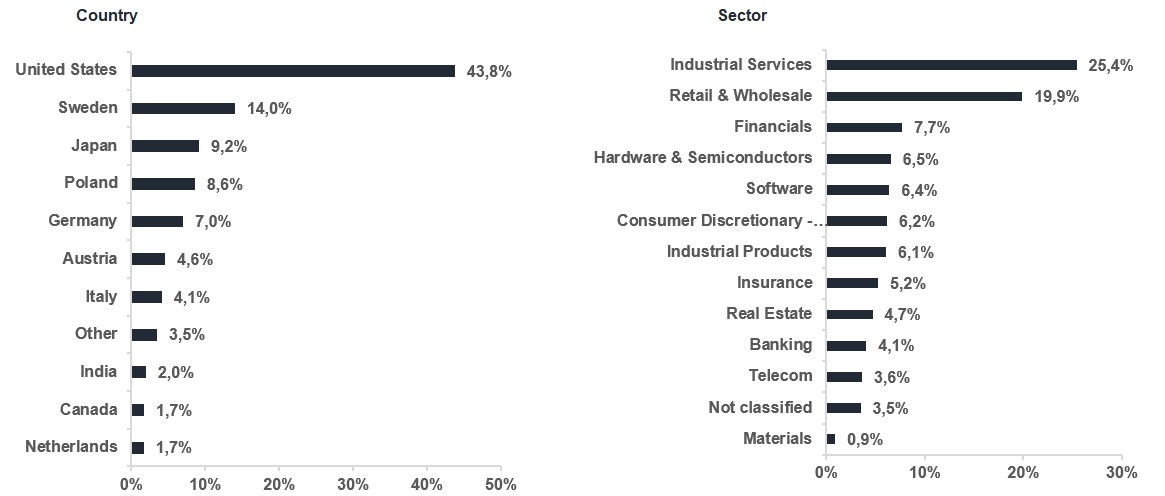

The fund now comprises 34 companies exposed to a range of sectors and geographies, with each company chosen on its own merits. We believe that a concentrated but also diversified actively managed small cap fund that focuses on stock picking has the characteristics to deliver great returns to unit-holders over time.

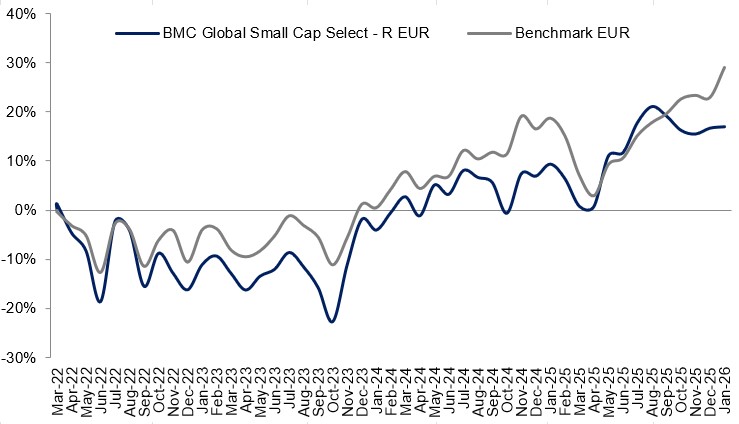

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

United Natural Foods

Catena

Allegro

Porr Group

NCR Atelos

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026