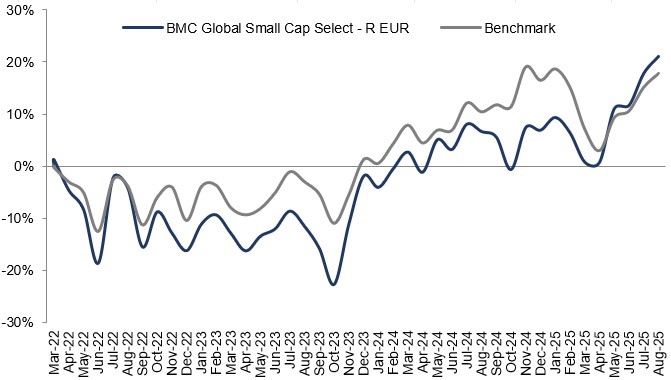

The strongest contributors to the fund's August performance were Blue Bird, US Lime & Minerals, and Legacy Housing, while the weakest were Palomar, IIFL Finance, and Griffon. August was an intensive reporting month in which many US holdings published their results for the second quarter. And again, most reported solid performances, although market reception on reporting day differed widely, with several of our companies seeing their share price rise or fall by more than 10%. Blue Bird (see our blog post on the company) was the largest positive contributor to the fund's return in August, managing tariff effects through price increases to see its results come in clearly above market expectations. The company also raised its long-term margin target by 200 basis points and launched a major share buyback program. Palomar, which had the biggest negative impact on the fund's return in August, also delivered a solid report, with a 43% rise in profits and a further increase in its full-year guidance. The market, however, chose to focus on the company's largest business, earthquake insurance, falling short of expectations and on lower reinsurance premiums—which benefit Palomar in the short term—bringing the risk of increased competition and price pressure in the future.

Key market events and trends

During August, small caps and their achievements were once again center-stage, even though a number of political maneuvers and geopolitical events affected parts of the market. Among these was Fed chair Jerome Powell's speech suggesting a rate cut is fully feasible in September. The message was greeted well by the equity markets, with rate-sensitive companies jumping for joy at the news. Meanwhile, Donald Trump continued to create uncertainty with, among other things, attacks on individual Fed members and comments on interest rates. His actions were completely at odds with the concept of an independent central bank, creating considerable volatility, not least in the currency markets, where the US dollar weakened further.

Portfolio changes

During August, we bought two new holdings, Nagarro and NCR Atleos, and sold four others. We sold our remaining shares in Alpha Group after the bid on the company that we wrote about in July. Asbury Automotive left our portfolio because we were unhappy with the company's capital allocation strategy of making further acquisitions rather than buying back its own shares, which are currently trading at low multiples. Cicor Technologies has seen its share price double since we bought it in April, while the company has also acquired a large bankrupt asset that we believe increases the operational risk in the short term. The operational performance of Enghouse Systems and its capital allocation have proven disappointing, and we see better investment opportunities elsewhere.

Below, we provide short descriptions of our new holdings:

Nagarro: An entrepreneurially driven Indian IT consultants with a customer base comprising leading global companies across a broad swathe of sectors. Following a spin-off, the company is now listed in Germany. The company has a history of high organic growth, double-digit operating margins, and robust cash flows, but it has traded down to single-digit profit multiples owing to accounting deficiencies, a weaker consulting market, and strong currency headwinds that overshadow the solid improvements in its results during the year.

NCR Atleos: The largest global supplier of hardware, services, and software for ATMs. Growth is driven by an increasing share of outsourcing of ATM services rather than the number of units installed, which means some 80% of revenues are recurring. After its spin-off in 2023 at high debt levels, the company has used its solid and predictable cash flows to amortize debt to more sustainable levels. This now allows it to take advantage of its low valuation by redirecting cash flows toward larger share buybacks.

The fund's positioning

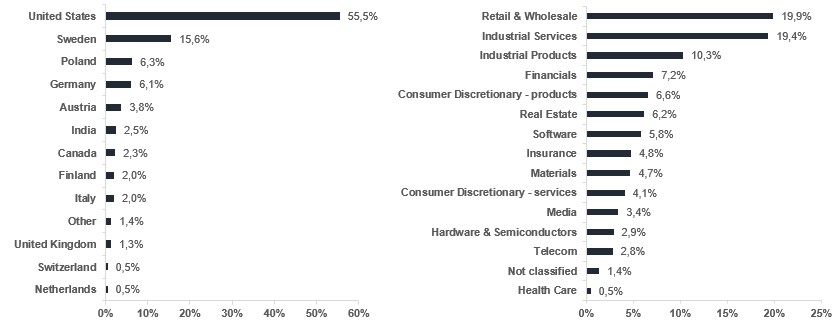

As in July, many of our US holdings again performed strongly in August, and thanks to this and further investments in existing holdings and our new positions in the above-mentioned NCR Atleos, the US portion of our fund is now around 55%. Although this is in the higher percentage range of what we have historically held, it remains underweight versus our benchmark index. We once again reiterate that the companies themselves are our chief focus when we investment, and whether we are over- or underweight in a geography or an industry is a reflection of the companies we have chosen to invest in rather than an active allocation decision. As always, we seek out companies with strong positions in industries with great future prospects. An example of this is the European consumer industry, which benefits from rate cuts and a weaker USD (as much of what the industry imports is priced in USD) and European and US construction and industrials companies, which are bolstered by large regional investments in infrastructure, data centers, defense, and industrial capacity.

*MSCI ACWI small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

Blue Bird

United States Lime & Minerals

flatexDEGIRO

United Natural Foods

First Advantage

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026