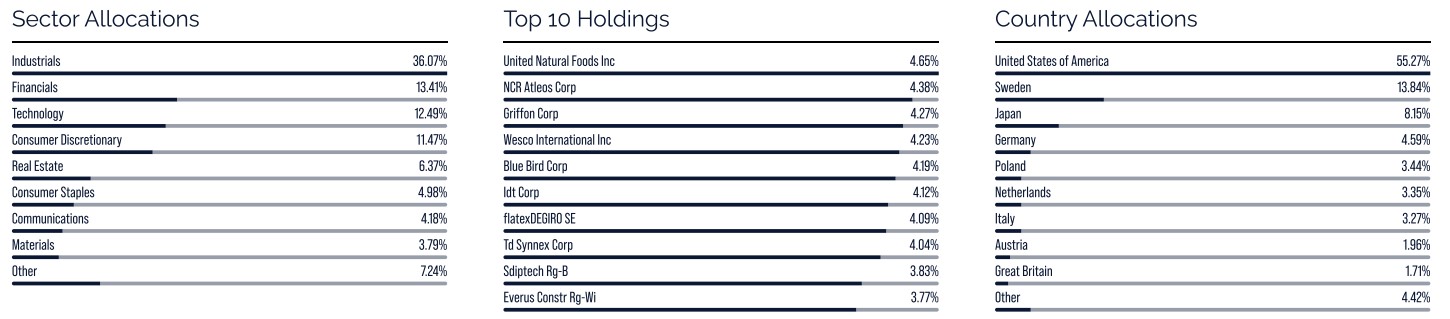

The strongest contributors to the fund's returns for April were Griffon, Wesco, and Ingram Micro, while the weakest were USLM, Climb Global, and NCR Atleos.

Although we saw no long-term resolution of the Middle Eastern conflict and we expect large ongoing disruption to the supply of oil and other key inputs, many of the world's stock markets set new records on expectations of de-escalation and hopes for a negotiated settlement. Many of our fund's holdings recovered all the declines in March and more besides during April, and the fund also reached new highs before a couple of weaker company reports at the end of the month dragged the fund's NAV down a little.

Of the strongest contributors, only Wesco has reported. The company's organic growth accelerated in the quarter and its margins continued to expand, driven by solid growth in data centers. Among the lowest contributors to the fund's returns, two companies issued weak reports: USLM, where we saw a downward trend in limestone prices for the first time in several years; and Climb Global, for which the significantly higher operating costs reduced profits y/y despite accelerating revenue growth.

Key market events and trends

MSCI World rose 9% in USD during April, its best monthly return since November 2022. The conflict in the Middle East contributed to a moderate pick-up in the oil price, but the bond and equity markets largely chose to ignore the geopolitical tumult.

Higher energy costs are likely to have an impact on inflation, burden economic activity, and weaken the already fragile consumer sentiment. Regardless, the markets chose to focus elsewhere. Consumers hold record-large savings that can be channeled to some extent into the equity markets.

The build-up of AI infrastructure continues apace and is accelerating, with semiconductors still the primary beneficiary of this expansion phase. In 2022, industry analysts predicted that the semiconductor market would reach annual revenues of USD 1,000bn by 2030. It now appears this level will be reached this year, with continued strong growth in 2027 before a slower pace is expected in 2028.

Company results corroborate this positive scenario. S&P 500 companies' profits for Q1 2026 were up by 28%, which was double the 14% expected at the start of the year. In Europe, Stoxx 600 companies saw profit growth of 7%, with cyclical consumption proving the most prominent factor. The automotive sector has recovered from its weak 2025, although this was cyclical rather than structural. European industry—to which our fund has good exposure—is seeing a more sustainable growth trend.

Despite the strong share price movements, valuations are attractive. Based on a forward-looking P/E of 18.5x for MSCI ACWI, forecasted profit growth of 28% in the USA, and the accelerating AI-driven revenues, the market is far from overvalued.

Portfolio changes

During April, we bought into four new holdings. Below, we provide short summaries of these.

Brink's: The world's largest cash/handling company, with around a 25% market share. Among its services are cash-in-transit, cash handling, and servicing of ATMs. The company is characterized by high entry barriers, long-standing customer relationships, and stable cash flows. Despite structural headwinds for cash, Brink's has delivered around 5% organic growth over time. Its transformative acquisition of NCR Atleos, which was also one of our holdings, has met with negative market reactions, despite the appealing valuation and considerable potential for synergies. As we wrote about the bid in our newsletter for February:

NCR Atleos, which is one of two global providers of hardware, service, and software for ATMs, delivered a solid year-end, with EPS growth exceeding 20% and robust cash flow. Unfortunately, Brink's, its sector competitor, took that opportunity to launch a bid. We are normally grateful for such bids, but we sense the company will be sold too cheaply. The bid, which comprises around 60% cash and 40% Brinks shares, represents around 10x NCR Atleos's expected net profit for 2026. There has previously been speculation about such a deal, even before NCR Atleos was spun off, but we believe this bid has come too soon after the company's independence. Given the increased outsourcing of ATM services, ongoing investment cycle for ATM upgrades, margin expansion, refinancing of expensive loans, solid cash flow for loan repayment, and the share buyback, we had expected the company to double its EPS in the coming three to four years.

Limbach: A US company focused on the installation and servicing of healthcare, industrial, and education facilities. Since its listing in 2016, the company has restructured from a sub-contractor to a turnkey contractor to having a direct relationship with property owners. This latter today represents 75% of its business and brings higher margins, with lower tied-up capital and less cyclicality. The restructuring has weighed down revenue growth in the short term, but thanks to a more balanced segment mix, organic growth should pick up again, while high cash conversion and a solid balance sheet allow for an active acquisition agenda.

Mersen: A French industrial company strongly positioned within electrical components and graphite products. Its Electrical Power business provides stable growth and rising margins, thanks to robust demand from data centers, while its Advanced Materials business is temporarily burdened by overcapacity owing to sluggish electric vehicle sales and poor demand for solar cells. Given new opportunities to fill capacity through growth in data centers and small modular nuclear reactors, growth should pick up in the coming years, while better capacity utilization and a completed investment cycle should improve margins and cash flows.

TD Synnex: Together with sector colleague Ingram Micro, which we bought into the previous month, TD Synnex is one of the world's largest IT distributors. The company is positioned for increased demand for AI infrastructure and a cyclical recovery in IT hardware. Its core business sees stable cash flows, economies of scale, and great pricing power. Moreover, we find a relatively hidden asset in the form of Hyve, a contract manufacturer for hyper-scalers like Meta and Oracle, in which it can realize considerable value through increased dissemination of information and a potential separate listing.

The fund's positioning

At present, the fund comprises 43 companies exposed to a range of sectors and geographies, with companies chosen on their own merits. We believe a concentrated but also diversified, actively managed small cap fund focused on stockpicking has all the prerequisites to deliver great returns to its unitholders over time.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

United Natural Foods

NCR Atelos

Griffon

Wesco

Blue Bird

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026