The best contributors to performance during the month were Heijmans, Porr Group, and FlatexDegiro. Those with the weakest performance in April were Covenant Logistics, Lindex Group, and Tutor Perini. The top contributors were again some of our larger holdings, delivering solid reports and providing optimistic guidance. Heijmans reported a stable Q1 with an expanding order book and high activity in all business areas, while at its capital markets day at the start of the month, Porr Group lifted its margin outlook, and FlatexDegiro's report came in far above market expectations on both trade and net interest income. At the other end of the scale, the picture was more fractured, with the weak performance of our US holdings Covenant Logistics and Tutor Perini stemming more from expectations of a negative impact from tariffs and a weaker domestic economy, while the Lindex Group share price fell sharply on a poor report with negative revenue and profit growth.

Key market events and trends (what has influenced performance most?)

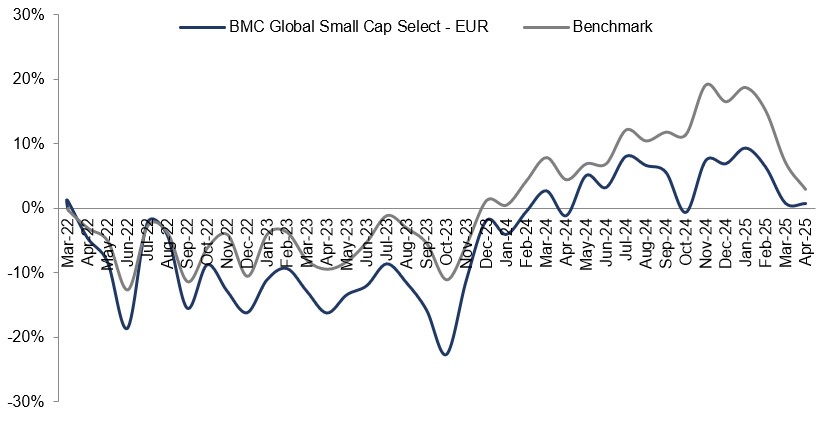

April was a month dominated by tariffs and the ongoing reporting season. Since April 2—the so-called "Liberation Day"—uncertainty regarding tariff levels and their consequences has remained high, but we have also seen many companies indicating a very limited impact so far. There is little hard data pointing to any major slowdown to speak of right now, except in terms of China–US trade itself and the transport sector in the US. Although the situation is volatile, there have been multiple indications in recent weeks of the tone calming down considerably. It is essential there is some form of agreement between China and the US, and we expect the stock exchanges to remain sluggish in the coming month, but also that the winners and losers will become increasingly clear as the new conditions settle in. We continuously work to position the fund to be full of such winners so that our unitholders can benefit from what is happening in the world.

Portfolio changes

Given that this market turbulence is creating opportunities, we have remained more active than usual and made more changes during this month than we usually do over this time. During April, we bought Alpha Group International, Cicor Technologies, Climb Global Solutions, and Note, and we sold A&W, Diploma, and Pluxee. We sold A&W as its underlying growth failed to live up to expectations; Diploma because its valuation stalled and we question its method of calculating organic growth; and Pluxee because we felt uncomfortable with the ongoing reappearance of regulatory risks. Below, we offer short descriptions of our new holdings.

Alpha Group International: A UK-based currency broker that specializes in helping companies and risk capital firms to manage their currency exposure and risk. A capital-light business that doesn't take any balance sheet risk and only acts as an intermediary and advisor. High double-digit organic growth with a 50%-plus operating margin; trading at low profit multiples.

Cicor Technologies: A rapidly growing and particularly profitable Swiss contract manufacturer with plants around Europe and satellites in the US and Asia. Benefits from several mega-trends, including outsourcing of production, electrification, and "reshoring" of manufacturing capacity. A goal of again doubling turnover in the next four years (around 20% CAGR) through a combination of organic and acquired growth.

Climb Global Solutions: US software distributor, primarily in cybersecurity and data centers, with organic growth driven by long-term and expanded collaboration with innovative developers of software solutions. Solid niche position in fast-growing markers, capital-light business with a high share of recurring revenues, and successful acquisition strategy leave us expecting many years of continued high profit growth.

Note: A rapidly growing and particularly profitable contract manufacturer with plants primarily in northern Europe. Benefits from several mega-trends, including outsourcing of production, electrification, and "reshoring" of manufacturing capacity. Growth target of around 15% per year through 2028, largely based on existing contracts and current pipeline, along with a smaller share of supplementary acquisitions.

The fund's positioning—our market expectations

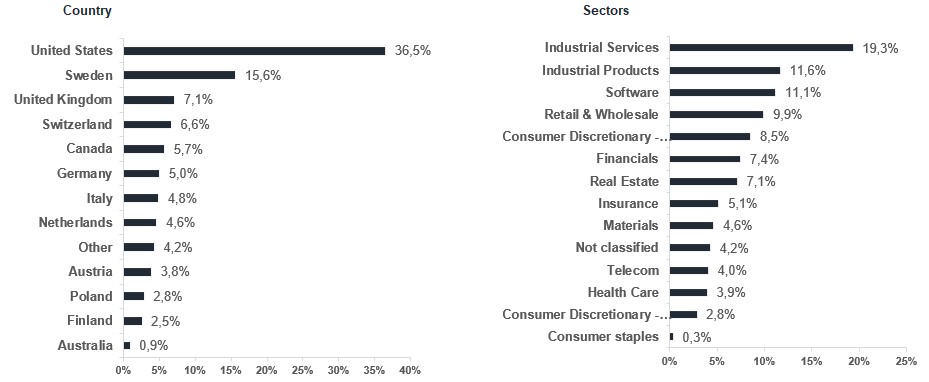

As active investment managers with a global mandate and a concentrate portfolio, we have the advantage of quickly being able to reallocate to adapt to new circumstances. We have reduced the fund's exposure to companies with a direct impact from tariffs and increased the proportion of those positioned well for secular growth trends, with recurring revenues and solid balance sheets. We maintain a relative underweight in the fund to the US and are investing in reasonably valued European companies.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

flatexDEGIRO

Heijmans

Truecaller

IDT Corporation

Siegfried

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026