The stocks that provided the best contributions to the fund during October were Vulcan Materials, Martin Marietta, and Nvidia. Those with the weakest performance were Atlas Copco, SIKA, and ASML.

We can connect the negative developments in ASML and Atlas Copco during the month with the generally smaller scale of the investments in the semiconductor industry. ASML had a tough time on reporting day, as the market disliked its order intake falling short of expectations and the company taking down guidance for 2025 sales. Our global team will attend ASML's capital markets day in mid-November to form an opinion on the company's future prospects. Keep an eye out for news on this both on LinkedIn and our blog. During October, we attended the capital markets day of SIKA (one of the fund's holdings) in Zürich. SIKA is a building materials company that operates at the forefront of quality infrastructure renovation, such as bridges and tunnels. By renovating rather than building new infrastructure, we can save enormously on the carbon emissions that would otherwise be produced from the manufacture of new concrete.

On the positive side, we saw major upturns from Vulcan Materials and Martin Marietta, both releasing quarterly reports that the market appreciated. Nvidia continues its solid performance thanks to all the AI investments.

Feel free to read our blog posts about our analysis trips and company meetings. You can find our blog here.

Key market events and trends (what has influenced performance most?)

The equity markets were volatile during October, affected by sizable swings in long-term bond yields and statements from China regarding economic stimuli. China is undertaking an expansive fiscal policy aimed at supporting the country's growth, including, among other things, debt cancellation, measures to aid consumers, and easing of banks' security measures so they can lend more. News of these economic stimuli has bolstered the Chinese equity market.

Inflation in the US continues to drop, leaving us anticipating a further cut in the policy rate of 0.25–0.5 percentage points before year-end. Despite falling inflation, the ten-year US treasury bond yield has risen by 0.5 percentage points to around 4.3%. Expectations of a deepening US budget deficit in the coming years, as Donald Trump won the presidential elections, lie behind the latest interest rate increase. Trump spoke widely in his election campaign about cutting corporate taxes, which would reduce the amount of tax the state receives. The rising market interest rates lessened the risk appetite for stocks during the month, and thus the appeal of investing in smaller companies.

Last month, we wrote that vehicle manufacturers in Europe were undergoing a minor crisis—and this has now widened into a greater quagmire. VW is now discussing the closure of three plants in Europe and making thousands redundant to cut its costs. The company is suffering from having been far too slow in transitioning its manufacturing to electric vehicles. Pure electric cars currently represent less than 10% of all vehicles rolling off VW's lines. China's BYD is now the world's largest electric vehicle manufacturer, with revenues surpassing Tesla's in the company's most recent quarterly report. All this drama among European vehicle manufacturers also affects the semiconductor industry, which supplies them with chips. As a result, companies like Infineon and ST Microelectronics have seen their stock prices plummet.

Portfolio changes

We made a few changes to BMC Global Select during October. We sold our Brazilian Special Situation, payment company Pagseguro. Its Special Situations replacement in the fund is Nike, the well-known US sports clothing company. Nike has had a tough time in the equity markets over the past five years owing to a mistake it made with its distribution model. It raised prices and focused more on exclusive distributors, which hampered its sales. To resolve this error, Nike has returned to clothing and shoes sales with a wider distribution and more retailers. Its valuation is at a five-year low and, assuming its earnings per share grow by more than 15% next year, we consider it a particularly interesting investment. We also dipped briefly into the US's Paypal during October but sold out of the company again after its questionable quarterly report.

The fund's positioning—our market expectations

Our global fund offers an exciting blend of solid Champions and thrilling Special Situations stocks. We expect the fall's rate cuts will prove a key trigger for returns in the future. A further positive factor for the equity markets is the end of the US presidential race, which we can now put behind us. At the time of writing, BMC Global Select sees forecasted aggregated profit growth of more than 16% for the coming year, which would contribute positively to the fund's future returns.

We thank you for your continued faith in us in investing your capital.

*MSCI All Country World NTR $ in EUR

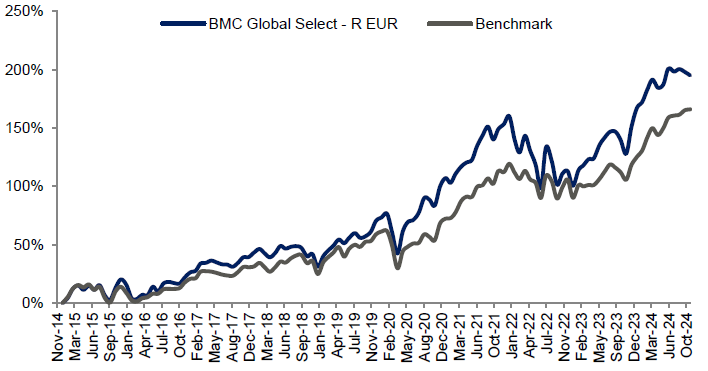

| 1 Mth | YTD | 3 Years | Since inception | |

| BMC Global Select Fund - R EUR | -1,01% | 10,50% | 18,51% | 195,03% |

| Benchmark (EUR) | 0,33% | 18,16% | 24,77% | 165,98% |

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

Vulcan Materials

ALPHABET

MARTIN MARIETTA MATERIALS INC

Progressive Corporation

ICICI Bank

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026