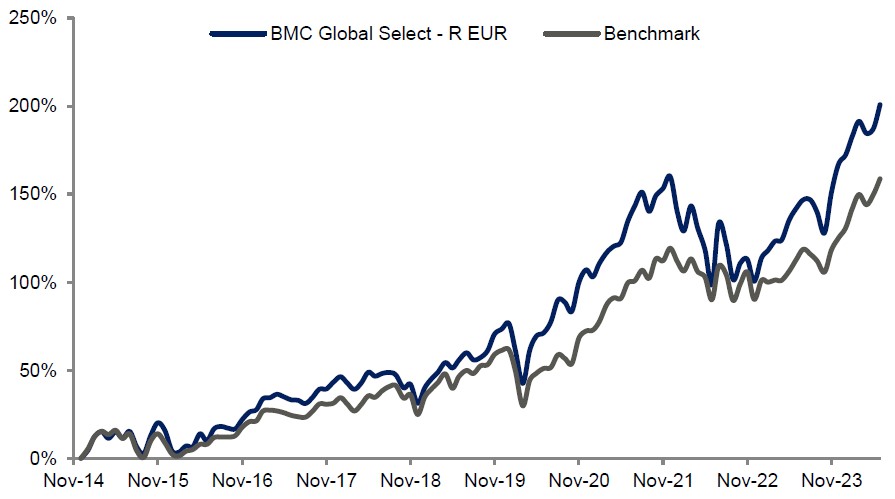

As we have stated in previous newsletters, the world is – from an economic perspective – doing well. The fund has risen by 12.66% so far this year, just as it should have done given how companies continue to grow their profits.

During June, a majority of the analyst team was in the US for, among other things, company visits in Texas and for the William Blair equity conference in Chicago. During these travels, we met both exciting new companies and some already in our portfolio for the visits we consider a key part of our investment process. On our website, you can find a blog post (in Swedish) about our trip to Chicago, along with a report on Fortnox's capital markets day. You can find our blog posts here.

Key market events and trends (what has influenced performance most?)

On June 6, it was time for the ECB to cut interest rates by 0.25 percentage points. It was the central bank's first cut in several years and proved a welcome boost for the equity markets. Now we await the US's Fed to make its first cuts. The US job market has proven incredibly robust, making it difficult for inflation to come down to really low levels. Fed boss Jerome Powell recently stated his intention for inflation to have come down towards about 2% before the Fed will make its first cuts.

Another trend affecting the stock markets is AI and all the associated tech investments. And yet another is the sale of electric vehicles. The EU is currently debating the level of tariffs on Chinese electric cars to incentivize European car manufacturing. China is skilled at making electric vehicles and is ahead of its European counterparts in both price and performance. This is one of the reasons why European vehicle manufacturers have such low valuations.

Portfolio changes

During the month, we sold Thermo Fisher, a holding we had owned for many years with a solid contribution to the fund. The company will, in all likelihood, continue its positive performance following our sale, but versus the rest of our portfolio, Thermo Fisher has borrowed a little too well when financing its acquisitions, meaning it will likely suffer from somewhat lower growth than we'd like in the years to come. We believe your capital would be better invested in the fund's other holdings, at least in the next two to three years.

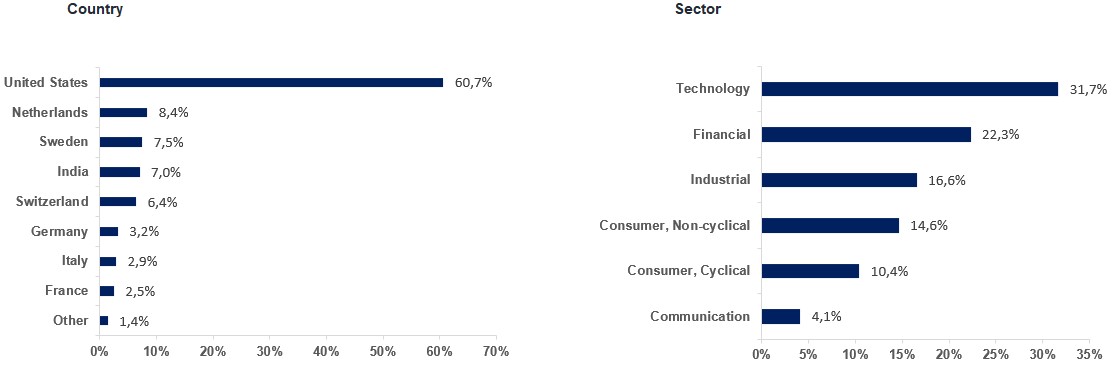

The fund's positioning—our market expectations

Our aim is to invest in a portfolio of the World's Finest Companies. We consider our current portfolio composition to be particularly strong and balanced. Our summer vacation typically comes early, and when you read this we will have returned from our break, ready for the exciting reporting season to begin—more on this in our next newsletter.

* MSCI AC World NTR USD (in EUR)

1 mth | YTD | 3 years | Since incep. | |

| BMC Global Select Fund - R EUR | 4.66% | 12.66% | 28,19% | 200,79% |

| Benchmark | 3.48% | 14.92% | 29,59% | 158,69% |

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

MARTIN MARIETTA MATERIALS INC

MICROSOFT CORP

ALPHABET

MASTERCARD INC

S&P GLOBAL

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026