The strongest contributors to the fund’s performance in the month were flatexDEGIRO, TSMC, and Kyoto Financial Group. Our Polish banks also performed well. Among the weakest contributors were SAP, Microsoft, and Sea Ltd.

We highlight flatexDEGIRO among the best performers, having seen its share price increase by more than 100% during 2025 and continue this robust performance this year, thanks to the trend among young people across Europe to increasingly trade online. This was raised as a desirable factor in the Draghi report and is an idea now supported by the governments of both Germany and Poland. The future for online brokers looks bright across Europe and especially so, we believe, for flatexDEGIRO. In Sweden, trading stocks and funds through an online broker is considered the obvious choice, but it has not been the same in many parts of Europe.

The three weakest contributors all have in common that AI’s success is now prompting the market to question the future for software companies. We have thus reduced our exposure to this industry. While we sold off Adobe a year ago, we also exited Cadence Design System during January. We consider SAP and Microsoft to be so difficult for others to challenge that we maintain our holdings, while Sea has several other legs to stand on beyond software/gaming. Although January was a tough month for these three stocks, we hold the same long-term positive view on these names.

Key market events and trends

January 2026 proved one of the most geopolitically turbulent starts to a year for a long time, with the kidnapping of Venezuela’s president, the US’s threat of military action in Greenland, and unrest in both Iran and Minneapolis.

The market moved in the opposite direction, however, with MSCI World increasing by 2.9% in dollar terms, while the dollar itself weakened by 1.4% against the euro—an indication that investors are currently positive regarding companies’ earnings outlooks for 2026. The weighted earnings forecast is for 10–14% growth, with US tech companies standing out at expected +27% growth. Company reports in January supported these expectations to an extent, although market reactions in individual stocks, such as Microsoft and SAP, were unexpectedly volatile versus what the companies actually delivered.

Gold and silver experienced almost parabolic rises in early January, only to plummet when the new Federal Reserve chair was announced as Kevin Warsh. The rapid decline also unleashed a deleveraging in products exposed to gold and silver, which further exacerbated the drop. The markets see Kevin Warsh as a stabilizing force, minimizing demand for assets that are seen as safe havens.

In February, we await a wave of company reports that will also include 2026 guidance. Indications suggest stable profit growth.

Portfolio changes

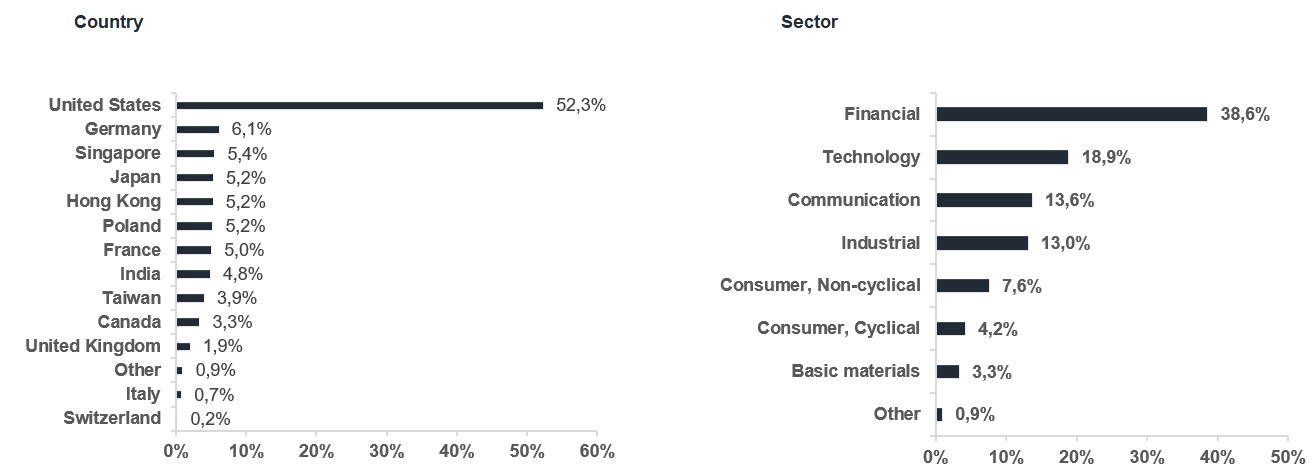

During the month, we sold Cadence Design System. This is a quality company, but we believe we have more than enough semiconductor companies in the fund. We also sold US insurance brokerage Arthur J Gallagher and bought Prudential, which has its primary insurance operations in more than 15 markets across Asia.

We took profits in two Special Situations, memory chip manufacturer Micron Technology and financial group Swissquote. In their wake, we invested further in companies in Asia. During 2025, we invested for the first time in Japan, and we followed up in January with two Champions in Hong Kong: Hong Kong Exchange and Prudential. These companies provide us with the right type of exposure to this region.

The fund’s positioning

Our strategy for the fund is to focus on investments in a collection of the world’s finest companies, with the addition of our more opportunistic Special Situations holdings. In 2025, we had a somewhat too large exposure to the US dollar and too little a share of the fund in Special Situations. We have now adapted the portfolio more to this changeable world and have a positive outlook for 2026. Both companies and governments are taking big bets, while interest rate cuts will help consumers, so it would take a lot for 2026 not to be a good year for investing.

*MSCI All Country World NTR $ in EUR

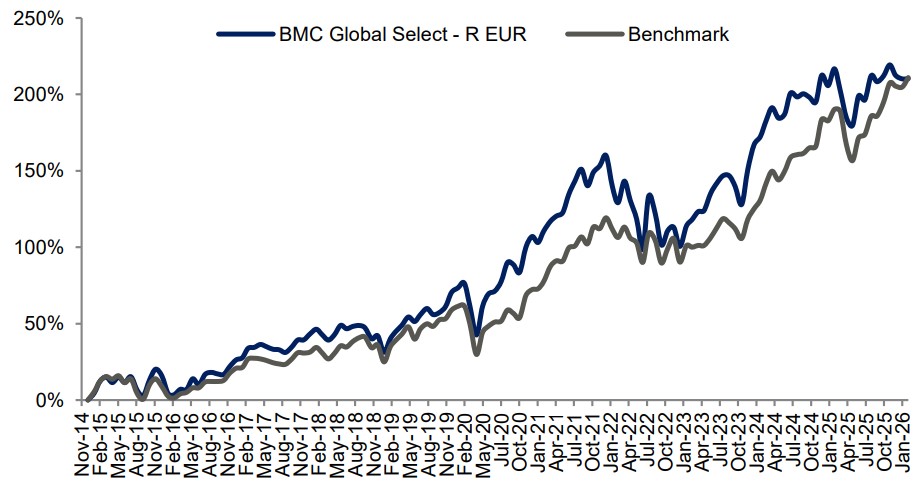

| 1 mth | YTD | five years | Since inception | |

| BMC Global Select Fund - R EUR | 0,04% | 0,04% | 52,78% | 210,29% |

| Benchmark (EUR) | 2,05% | 2,05% | 79,97% | 211,02% |

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

ALPHABET

Amazon

NVIDIA CORP

TSMC

MASTERCARD INC

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026