The stocks that contributed most strongly to the fund's performance in the month were TSMC, Kandenko, and Wheaton Precious Metals, while the weakest contributors were FlatexDEGIRO, Amazon, and Charles Schwab. Among the market movements, we want to highlight Kandenko, which is one of the Japanese installation companies constructing datacenters in the country. We had an instructive meeting with the company's CFO when we visited Tokyo before Christmas, and we believe the company has at least three to five years of strong growth ahead of it. However, the month also saw FlatexDEGIRO and Charles Schwab—both online share and fund brokerage platforms—impacted by disruptive AI sentiment that threw a wet blanket over many names around the world, from software firms to online brokers and banks. We note, however, that FlatexDEGIRO's share price has picked up since the end of February.

Key market events and trends

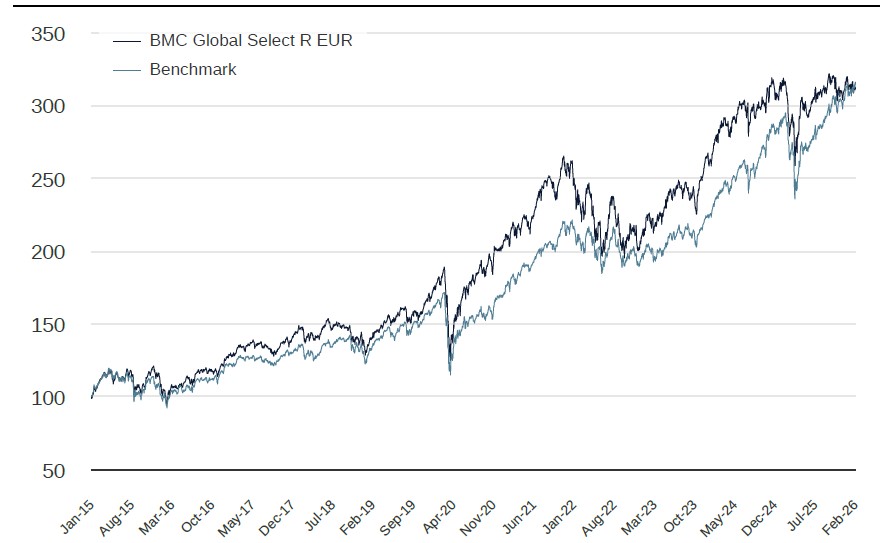

The MSCI World index is nearing an all-time high, but a significant rotation is going on under the surface, with a striking spread in performance. Software stocks have dropped by around 20% this year, while oil companies have seen their share prices rise by some 30%—even before the conflict between Israel, the US, and Iran intensified towards the end of February. The geopolitical environment has changed markedly and remains hard to predict.

Despite this, the stock market reaction has been more rational than could have initially been expected. Investors are actively repricing geopolitical risk, AI-driven disruption, and structurally higher energy costs. In the software sector, it is too early to draw conclusions about the long-term impact of AI, but given the high valuations, some normalization was necessary. The strength of the oil sector reflects the need for producers to both accelerate the development of new fields and extend the lifetime of existing sites.

On the profit front, Q4 2025 reports and company guidance for 2026 offered solid foundations. Profit estimates for the large indices have been revised upward by 1–3% since the end of January, with expected profit growth for 2026 now at just over 10%. Europe stands out as especially positive, thanks to rising profit revisions, driven by increased activity within the construction and industrial sectors, plus policy initiatives that strengthen regional competitive power and defense.

Portfolio changes

We made change to a Japanese holding in February, taking a substantial profit in Kyoto Financial Group, which had seen its share price move from very cheap when we bought in last fall to more fully valued. We filled this gap by investing in a new Japanese Special Situations stock, Kyocera, in which we see much greater upside thanks partly to operational changes but also due to its large share buyback program. Japan and Korea are particularly interesting markets for us to invest in, offering many companies with considerable internal improvement potential.

We also took a small position in SK Hynix, a Korean memory manufacturer. Part of the rationale behind this was that we find the share price cheap, since it is expected to create around 70% of its entire market cap in profits in the next three years. But we also see upside if and when the company is listed on the US stock market, since there is a sizable valuation gap between SK Hynix and its US competitor Micron, which trades at around double the valuation. As memory chips are a volatile sector, we have initially taken a small position that we look forward to expanding over time.

In the tech part of the fund, we have decided to focus our software investments on Microsoft and take a break from SAP until we better understand how AI can impact a business systems company like SAP. Instead, we have invested in France's Schneider Electric, one of the world's best engineering companies, which holds a robust position particularly in low- and medium-voltage substations and other energy-automization and distribution products. We have long wished to hold this excellent company and could now buy in at a good valuation.

The fund's positioning

The fund now comprises 34 companies exposed to a range of sectors and geographies, creating a diversified portfolio of fine companies with solid balance sheets and high profit growth. We are convinced these will prove over time to be a recipe for growth for you, our unitholders, in building your long-term capital.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

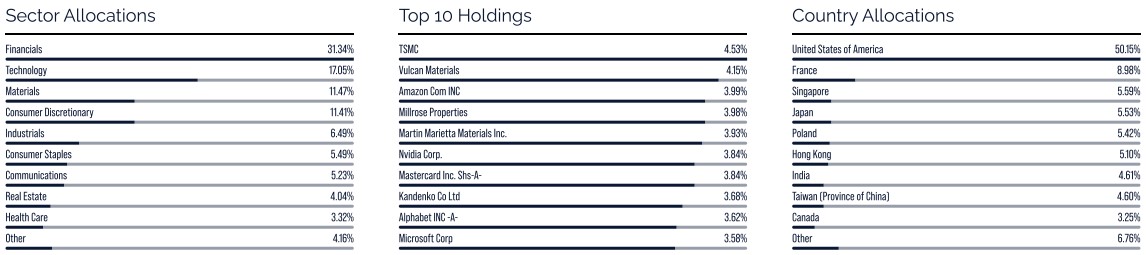

TSMC

Vulcan Materials

Amazon

Millrose Properties

MARTIN MARIETTA MATERIALS INC

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026