The stocks that offered the best performances for the month were Progressive (vehicle insurance) and Ferrari, while Vonovia (German real estate) also did well. Of these, we highlight Vonovia as particularly interesting. The company has not really had the same refinancing problems as other real estate companies and, in our view, Vonovia's share price drop (from EUR 50 to EUR 20 per share) between 2022 and 2023 was a severe overreaction with a very short-term focus by the market. We bought into the share in August 2023, when it was trading at around half its book value, and have now positioned ourselves for what we expect to be its journey to where it should typically trade (around book value, which is currently EUR 44 per share). Vonovia does not belong to the category of World's Finest Companies, but the market was offering a Special Situations stock that we wanted our unitholders to be part of.

Looking at the negatives during the month, we find construction materials companies Martin Marietta and Vulcan Materials, which delivered weaker quarterly reports, largely owing to poor weather conditions (heavy rain) in the US. We are not meteorologists, but experience tells us that construction not carried out during bad weather is often undertaken when the conditions improve, and so, as with Vonovia, it is preferable to hold firm and await improvements.

Key market events and trends (what has influenced performance most?)

A general semiconductor frenzy has gripped the market in recent months and debates rage about how whether and how far investments in artificial intelligence (AI) will be sufficiently profitable to match the levels of capital being invested. At the time of writing, one of our fund managers and an analyst are traveling in California to meet NVIDIA, Tesla, Cadence, Broadcom, Salesforce, and others to read the signs they give about investments in AI, among other things. Our narrowing of the fund's semiconductor exposure this summer seems to have been the right call as semiconductor companies have had a challenging time so far this year. We want to emphasize, however, that semiconductors are a rapidly growing industry, and so even though we have reduced our exposure, we will see them pick up again in the foreseeable future. During the summer, we also saw the Japanese stock market plummet. We do not hold any stocks there and the market movements have had more to do with "carry trades" stuck in a deadlock than any fundamental issues with the Japanese economy. The beauty of this is that the subsequent volatility has made it even more likely that interest rate cuts in developed market countries will now come sooner and stronger than was the case before this correction.

Portfolio changes

We made no changes to our portfolio during August.

The fund's positioning—our market expectations

The latter half of the summer has been quite messy on the stock markets, but we believe this turbulence has accelerated the US's first rate cuts. In our view, interest rate cuts are likely on an ongoing basis during the fall, starting from September. Many of the stocks that performed poorly during the summer, such as semiconductors and engineering, will benefit from lower rates in the future. Our view is that we have a portfolio of the World's Finest Companies that will continue to perform robustly during the fall.

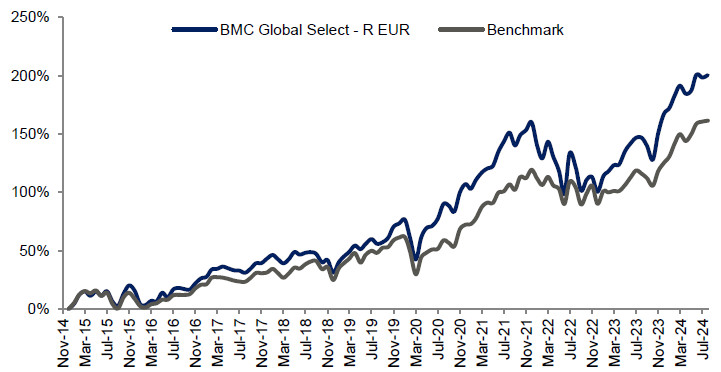

| 1 mth | YTD | 3 years | Since inception | |

| BMC Global Select - R EUR | 0,69% | 12,51% | 19,65% | 200,40% |

| Benchmark (EUR) | 0.30% | 16,11% | 26,42% | 161,39% |

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

Progressive Corporation

S&P GLOBAL

MASTERCARD INC

SIKA

Vonovia

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026