The strongest contributors to the fund’s returns during the month were Analog Devices, Euronext, TSMC, while at the other end of the scale, the weakest were FlatexDEGIRO, AMD, and Amazon.

During February, we saw extensive share price drops in the software sector that look set to go down in history as the most severe—an epoch that is now referred to as “SaaSpocalypse” or “SaaSmageddon.” At the same time, the semiconductor industry continued its upward trajectory, leading to a historically large gap between the two sectors. The drop in the software sector, spurred by Anthropic’s launch of Claude Cowork, accelerated dramatically after the company launched further niched products for the legal, financial analysis, and HR fields. Several other sectors saw share prices fall as a result, with the market questioning which would be next. We chose to increase our holdings in some of the companies we believe will be particularly hard to disrupt with AI but that have seen their share price take a hit as this irrational selling gathered pace. We also chose to sell some software holdings, especially those we expect to face the greatest challenges. We don’t consider our investments as perpetual, and we act when we see a significant shift in the market.

The dust started to settle at the end of February, and we see the early signs of a recovery in the software sector, although there are sizable differences between companies. This affirms what we wrote in the previous month’s newsletter, that the wheat will be sorted from the chaff, making it harder to speak about “software” as a sector seeing homogenous development among companies in the future.

Meanwhile, the strong performance continued for the fund’s hardware and semiconductor companies, which issued solid reports. Not least Broadcom and Arista Networks. Broadcom beat expectations by a wide margin, raising its guidance for AI chips to more than USD 100bn for 2027. During 2025, its revenues in this segment were around USD 20bn, meaning it expects to more than double these revenues for two years in a row. This explosive performance is the result of customers’ strategies to accelerate their own development of AI chips so as not to be dependent on Nvidia. Arista Networks, which provides network equipment for datacenters, also beat expectations and raised its full-year guidance to more than 25% growth.

Another solid contributor in February was Netflix, which saw its share price up 30% after the company threw in the towel on its quest for Warner Bros after Paramount outbid it. We appreciate this move as we believe the company has great opportunities to grow organically.

Key market events and trends

The MSCI World index is nearing an all-time high, but a significant rotation is going on under the surface, with a striking spread in performance. Software stocks have dropped by around 20% this year, while oil companies have seen their share prices rise by some 30%—even before the conflict between Israel, the US, and Iran intensified towards the end of February. The geopolitical environment has changed markedly and remains hard to predict.

Despite this, the stock market reaction has been more rational than could have initially been expected. Investors are actively repricing geopolitical risk, AI-driven disruption, and structurally higher energy costs. In the software sector, it is too early to draw conclusions about the long-term impact of AI, but given the high valuations, some normalization was necessary. The strength of the oil sector reflects the need for producers to both accelerate the development of new fields and extend the lifetime of existing sites.

On the profit front, Q4 2025 reports and company guidance for 2026 offered solid foundations. Profit estimates for the large indices have been revised upward by 1–3% since the end of January, with expected profit growth for 2026 now at just over 10%. Europe stands out as especially positive, thanks to rising profit revisions, driven by increased activity within the construction and industrial sectors, plus policy initiatives that strengthen regional competitive power and defense.

Portfolio changes

During February, we sold five holdings and bought into four new ones. Those we sold were software companies: Lime, Veeva, Intuit, Salesforce, and Zillow. The fund’s new holdings are Mediatek, SK Hynix, Schneider Electric, and Apotea.

Mediatek is a Taiwanese semiconductor company that primarily designs chips for smartphones. More recently, the company has expanded into the market for datacenters, largely by helping Google to design its own AI chip, a TPU. This year, Mediatek expects revenues of more than USD 1bn from this, which we believe it can scale up to several billion in the coming years, growing as a share of overall revenues. We thus anticipate promising growth in the coming years, as well as a revaluation of the company from the current level of 18x P/E (two years ahead).

Schneider Electric is a French industrials company within energy technology, with roots stretching back to the 1800s. It benefits from the overall electrification trend and the construction of datacenters in particular. The company provides essential power supply equipment for datacenters, also offering the cooling equipment that is increasingly important for newer facilities. Its largest market is the US, while Europe and India will see rapid growth in the coming years as the expansion of datacenters broadens.

South Korea’s SK Hynix is the world leader in the manufacturing of the advanced HBM (high bandwidth memory) chips. As a key supplier to Nvidia, it controls around 60% of the market.

Apotea is a Swedish online pharmacy with a business model driven by efficiency, tech, and automization. The company is steered by a highly engaged and skilled CEO, Pär Svärdson. In the wake of its weaker Q4, temporarily weighed down by rising costs, we anticipate ongoing growth opportunities and share price upside.

The fund’s positioning

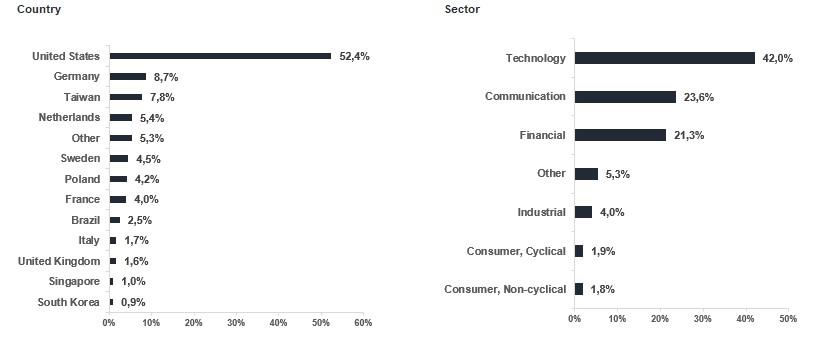

The fund currently comprises 36 companies exposed to a range of sectors, geographies, and driving forces but selected on their own merits. Overall, the portfolio has high forecast profit growth of 26% for the coming year. Our fund is also appealingly valued at a P/E of 21x, which represents a PEG ratio (valuation in relation to profit growth) of less than 1x. We believe that a concentrated but also diversified, actively managed global technology fund that focuses on stock picking has the characteristics to deliver great returns to unitholders over time.

We thank you for your continued faith in us in investing your capital.

*MSCI All Country World NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI All Country World Daily Index (NTR), and is calculated according to the "high watermark" principle.

NVIDIA CORP

MICROSOFT CORP

TSMC

WARSAW STOCK EXCHANGE

Schneider Electric

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026