In February, the strongest contributors to fund performance were NCR Atleos, Takasago Thermal Engineering, and Kandenko, while the weakest were FlatexDEGIRO, Climb Global Solutions, and Nagarro.

February was a month of end-of-year reports and general AI concerns. A majority of the fund's holdings have now reported their full-year numbers, and overall, these have been in line with or better than market expectations. At the same time, some of the fund's holdings have been hit by AI concerns, which are striking far and wide right now as the rapid developments within AI render certain business types obsolete or subject to extreme competition, with lower profitability as a consequence. The companies in the fund that have seen large share price drops not attributable to company-specific news include tech firms offering elements of software, web-based business, or IT consulting.

The best contributor in February, NCR Atleos, which is one of two global providers of hardware, service, and software for ATMs, delivered a solid year-end, with EPS growth exceeding 20% and robust cash flow. Unfortunately, Brinks, its sector competitor, took that opportunity to launch a bid. We are normally grateful for such bids, but we sense the company will be sold too cheaply. The bid, which comprises around 60% cash and 40% Brinks shares, represents around 10x NCR Atleos's expected net profit for 2026. There has previously been speculation about such a deal, even before NCR Atleos was spun off, but we believe this bid has come too soon after the company's independence. Given the increased outsourcing of ATM services, ongoing investment cycle for ATM upgrades, margin expansion, refinancing of expensive loans, solid cash flow for loan repayment, and the share buyback, we had expected the company to double its EPS in the coming three to four years.

The worst contributor in the month, FlatexDEGIRO, was initially traded up to record levels early in February, only to plummet sharply. This drop was spurred by news that AI can automatize certain advisory services, such as the basis for tax calculations, which are often provided as an optional extra by online brokers. These extras have typically seen only a marginal impact on the total, however, and they are largely non-existent in FlatexDEGIRO's case. Nevertheless, the company found itself in the category of those businesses being competed out by AI. The share price decline was then exacerbated by the proposal by Dutch politicians that the country implement a new capital taxation, which, if it passes, will mean both realized and unrealized (!) gains will be taxed at 36%. The Netherlands is FlatexDEGIRO's largest market, and this reform will, if implemented, prompt a marked reduction in trading and investment in equities and similar instruments. The proposal has met strong opposition, however, and we see that those proposing it have already conceded that it is somewhat unreasonable. Most likely, we will see a watered-down version of this tax reform implemented towards the end of December, something more stringent that current regulations but that does not eliminate all incentive to trade and invest in equities. FlatexDEGIRO also delivered its year-end 2025 results and initial guidance for 2026. We already knew that 2025 had been a great year, as the company's KPI report showed high activity towards the end of the year. And even though the initial 2026 guidance for 5–15% EPS growth did not meet market expectations, we know the company tends to be especially careful with its initial guidance, meaning it is reasonably likely that it will revise up its growth expectations during the year.

Key market events and trends

The MSCI World index is nearing an all-time high, but a significant rotation is going on under the surface, with a striking spread in performance. Software stocks have dropped by around 20% this year, while oil companies have seen their share prices rise by some 30%—even before the conflict between Israel, the US, and Iran intensified towards the end of February. The geopolitical environment has changed markedly and remains hard to predict.

Despite this, the stock market reaction has been more rational than could have initially been expected. Investors are actively repricing geopolitical risk, AI-driven disruption, and structurally higher energy costs. In the software sector, it is too early to draw conclusions about the long-term impact of AI, but given the high valuations, some normalization was necessary. The strength of the oil sector reflects the need for producers to both accelerate the development of new fields and extend the lifetime of existing sites.

On the profit front, Q4 2025 reports and company guidance for 2026 offered solid foundations. Profit estimates for the large indices have been revised upward by 1–3% since the end of January, with expected profit growth for 2026 now at just over 10%. Europe stands out as especially positive, thanks to rising profit revisions, driven by increased activity within the construction and industrial sectors, plus policy initiatives that strengthen regional competitive power and defense.

Portfolio changes

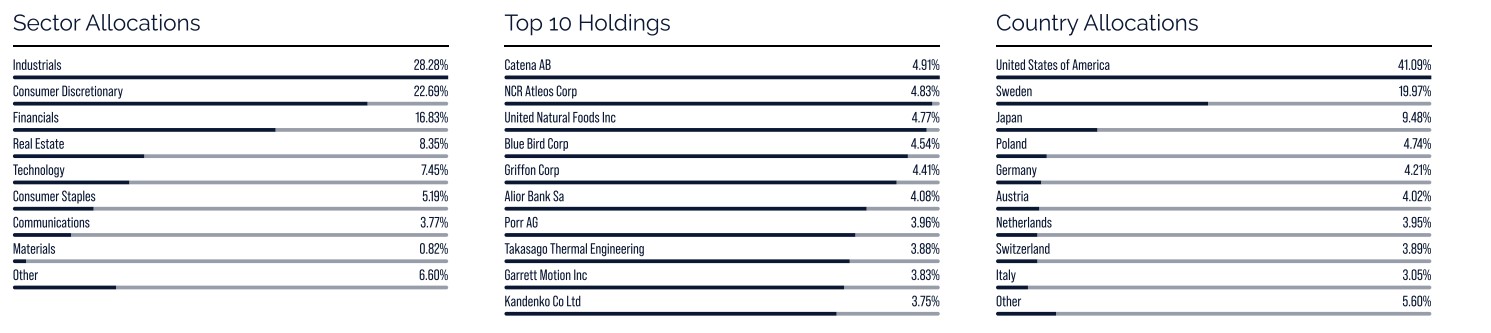

During the month, we bought BAM Group, Garret Motion, Warsaw Stock Exchange, and Intea Fastigheter. And we sold Everus, which had seen a solid performance since we bought in shortly after its separate listing in fall 2024. A US construction firm operating primarily on the electrical side, Everus has benefited from the enormous investments into datacenters. Following its year of high growth, margin expansion, and record-high profit margins, we see better risk-adjusted return potential elsewhere. Below, we offer short summaries of our new holdings.

BAM Group: A leading European construction company with robust positions in the Netherlands, the UK, and Ireland, thanks to a broad exposure to infrastructure, public projects, and housing. After several years of restructuring, the company has cut its share of loss-making projects substantially. Thanks to better risk control and cost discipline, its current order book is stronger than ever and with good execution, the company looks set to continue growing its revenues and expanding its margins. It currently sits on a significant net cash position; adjusted for this, the share price trades at around 8x profit.

Garret Motion: A US provider of turbochargers for the global vehicle industry. The company is growing thanks to turbochargers being included in an increasing number of combustion engine vehicles in order to boost engine efficiency and also by taking market share in new car models. At the same time, it invests 20–25% of its cash flow in product development for electric vehicles and industrial HVAC applications, including datacenters. Despite its entrenched market position, high profitability, and solid cash flow for share buybacks, the share trades at around 10x free cash flow owing to the market's skepticism regarding cars with combustion engines.

Warsaw Stock Exchange: The owner of the Warsaw stock exchange, GPW has a monopoly in the trading of equities, commodities, and related instruments in Poland. The Polish stock market has developed quickly, but it still trades at a significant discount and its market cap as a percentage of GDP is just over 20%, far below the EU average of some 65% and Sweden's 170%. The implementation of investment savings accounts, a compulsory savings program, large capital surplus among households, and plans to list several state-owned companies imply the foundations for a robust stock exchange, with increasing trading volumes for many years to come.

Intea Fastigheter: A Swedish social housing company focused on owning and developing real estate primarily for the judiciary and higher education. Around 95% of its customer base comprises public authorities and other public entities, with long, CPI-indexed rental contracts. The company is expected to raise rental income by up to 60% over the next five years through projects under development or starting in the coming years. Its balance sheet is solid, with further growth potential through acquisitions and new project starts.

The fund's positioning

The fund now comprises 37 companies exposed to a range of sectors and geographies, with companies chosen on their own merits. We believe a concentrated but diversified, actively managed small cap fund focused on stockpicking has all the prerequisites to deliver great returns to its unitholders over time.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

Catena

NCR Atelos

United Natural Foods

Blue Bird

Griffon

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026