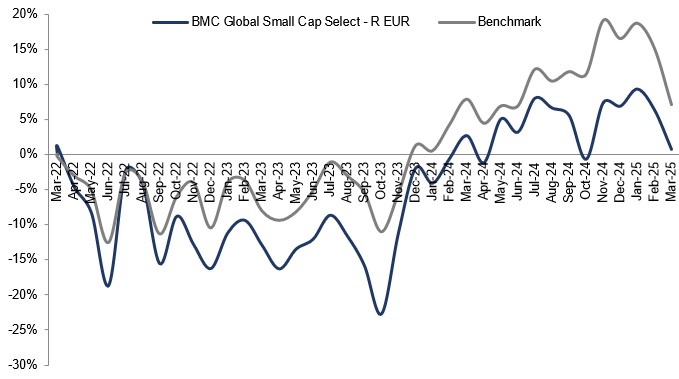

The stocks that contributed the best during the month were Fortnox, flatexDEGIRO, and Revo Insurance. Those with the weakest contributions during March were Covenant Logistics, Asbury Automotive, and United Parks & Resorts.

March was an intensive month on the reporting front, with many of our European companies filing their end-of-year reports for 2024. Fortnox, the portfolio holding providing the best contribution to the fund's performance in March, didn't report but was the subject of a takeover bid. On the last day of the month came the announcement that Fortnox's largest shareholder, Olof Hallrup, had, together with EQT, submitted a takeover bid at a some 40% premium to the previous trading day's closing price. Although it stings to have to say goodbye to the company, which is the epitome of a Champion, with its dominant position in a niche market, robust pricing power, high customer growth, scalable cost base, stellar cash conversion, solid balance sheet, and more, we are, of course, grateful that this frees up some cash in these turbulent times that we can invest in other holdings that we find to be trading at appealing valuations.

At the other end of the scale, we have seen further negative sentiment around many of our US companies. Despite the lack of company-specific news, we have seen several companies dropping by 5% or 10% in share price in March.

Key market events and trends (what has influenced performance most?)

Market uncertainty continued in March, with geopolitics and tariffs highest on the agenda. Both political opinions and real-life events affected the stock markets during the month and although the underlying sentiment has been negative, there are also many companies that will benefit as the playing field is redrawn. Some general observations from our many company visits in recent weeks:

As we said in last month's newsletter, when events make the markets jittery and turbulent, it often creates opportunities for us as active investors. Sometimes these are minor events, and other times they are enormous ones that can prompt interesting new trends, and so we are ready to take advantage of the investment opportunities that materialize. We maintain the fund's relative underweight in the US while we invest in reasonably valued companies driven by secular trends in Europe.

Portfolio changes

With the market turbulence creating decent buying opportunities as most companies are traded down across the board and their underlying performance disregarded, we have been more active than usual, making more changes during a single month than we would typically do over a longer time. It is also not impossible that April will again prove a transformational month, as we still see many super buying opportunities out in the market.

During March, we bought Porr Group, Revo Insurance, Swedencare, Truecaller, and Tutor Perini, while we sold Eurogroup Laminations, Text, VBG Group, and Vitec. We had also started building a position in a couple of European companies that will benefit from increased industrial activity. We aim to reveal these in our next newsletter. We sold Vitec to make space for Truecaller, which is growing organically more rapidly than Vitec even when including acquisitions, has considerably higher profitability (ROCE), and is valued lower. The other three holdings sold in March were ones we have consistently been reducing for a long time. Common among them is lower activity by customers, leading to weaker development in turnover and margin pressure, and we see no signs of improvement in the near term.

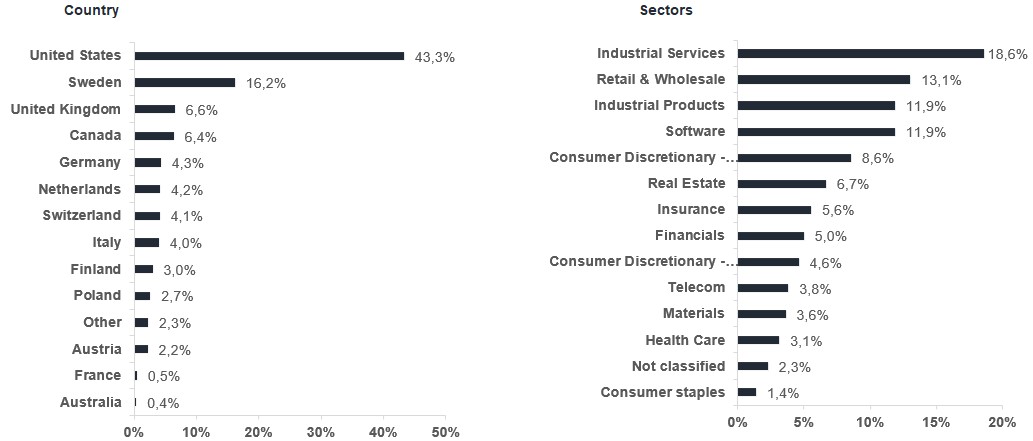

Porr Group: One of the leading construction companies in Central/Eastern Europe, which will benefit from large infrastructure and modernization initiatives in Europe. A larger increase in turnover notwithstanding, we expect solid profit growth in the coming years thanks to margin improvements (EBIT margin improving from today's 2.6% to >3.5%) and the company paying off expensive financing with its healthy cash flows.

Revo Insurance: An insurance company that has, thanks to its high digitalization pace, quickly grabbed market share in the underpenetrated market for Italian small and medium-sized enterprises. In only a short time, the company has achieved critical mass in premiums written and given ongoing high growth and incrementally higher margins, we expect many years of elevated profit growth.

Swedencare: An animal health company that has expanded substantially through expensive acquisitions. Leaving aside its poor M&A history, we see a healthy company showing double-digit organic growth, solid margins, high cash conversion, a steadily improving balance sheet, and, after a share price fall of more than 70%, an appealing valuation.

Tutor Perini: A US construction company focused on large-scale infrastructure projects and complex buildings. Its order book is nearly five times its turnover, leaving it expecting robust profit growth for the coming years. In only a short time, it has gone from high indebtedness to almost sitting on net cash. This, combined with solid cash flows, means we expect large share buybacks in the future.

Truecaller: A company that has developed a mobile app for safer communication. The narrative around the company is changing from it being an "Indian advertising company" to a "global SaaS firm within communication security." Thanks to its large and growing user base, increasing monetization, and scalable business model, we expect many years of high profit growth.

The fund's positioning—our market expectations

Given appetizing valuations, both relative to large caps and in absolute terms, our belief in small caps as an asset class is positioned for a period of relatively solid returns. We have taken advantage of the latest turbulence to bolster the quality among our Champions and to increase the share of Special Situations to ensure the fund is positioned for when the uncertainty tails off. Right now, macroeconomics are guiding share price movements and individual companies are, regardless of their performance, trading largely in tandem. Soon we will head into a new reporting season, when it will once again be company performance that steers share prices.

*MSCI ACWI Small Cap NTR $ in EUR

* The performance-based fee is 10% of the part of the total return that exceeds a so-called return threshold defined as the MSCI ACWI Small Cap Index (NTR), and is calculated according to the "high watermark" principle.

flatexDEGIRO

Heijmans

REV Group

IDT Corporation

Legacy Housing

Riskinformation

Past performance is not a guarantee of future returns. The value of shares in the fund may go up or down, and an investor may not get back the amount originally invested

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 8 jul 2026

Monthly Newsletter | 7 jul 2026